what is responsive investing?

Responsive Investing (RI) is best described as an alignment between an organization’s investments and its values. This concept is often referred to as a “double bottom line,” in which an investor integrates both financial and social criteria into their decision-making with the goal of seeking positive return in each. Social return criteria can include a wide range of elements, including environmental interests, moral values, and investing for the common good.

At FEG, our mission is to help clients achieve excellence as stewards of investment assets. We define the integration of values as “responsive” to recognize the range of interests across investors, rather than to suggest a homogenous definition for all investors. Decades of experience with Responsive Investing have shown that each investor brings to the table a unique mission and distinct set of values and principles that can help inform their investment strategy.

There are several broadly recognized definitions under the umbrella of Responsive Investing.

SOCIALLY RESPONSIBLE INVESTING (SRI)

A forerunner to today’s ESG-based strategies, SRI most often utilizes negative screening methodology—for example, excluding companies viewed as “sin stocks” in a portfolio—ideally without sacrificing market rate returns.

ENVIRONMENTAL, SOCIAL, AND GOVERNANCE (ESG)

ESG is typically used to describe an investment approach focused on these three broad aspects in a company. Notably, adopting an ESG lens does not require an investor to focus equally on all three areas; investors may choose to focus on one or more of these factors at their preference—e.g., environment. Many investors view ESG relative to the Principles for Responsible Investing (PRI)’s Sustainable Development Goals (SDGs), which were originally developed in 2015.

FAITH-BASED OR FAITH-DRIVEN INVESTING

Faith-based denotes investor communities seeking to integrate and promote specific values of their faith group—e.g., Catholic, Christian, Jewish—as part of their investment strategy. Some faith groups also utilize socially responsible criteria to broadly define their investment philosophy.

DIVERSITY, EQUITY, AND INCLUSION (DEI)

DEI represents another lens for investors to consider as they align their values with their portfolio. Some investors view this as a specific area of interest and establish clear DEI goals/targets, while others view it within the broader context of the social and governance elements of ESG.

Given its rapid growth and multifaceted nature, it is important for investors to have a clear understanding of what constitutes Responsive Investing and how they can implement these strategies into their own portfolio to ensure alignment between their investments and their values.

Increased Investor attention

RI INCREASES SHARE OF OVERALL INVESTMENT UNIVERSE

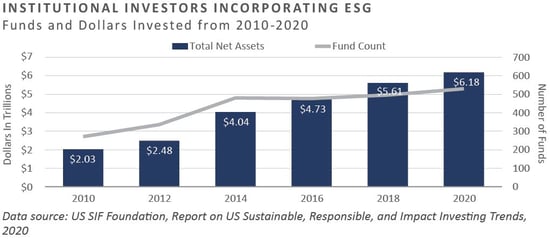

One measure of the growth in RI comes from the US SIF Foundation. In a 2020 report, they identified $16.6 trillion in U.S.-domiciled assets held by 530 institutional investors, 384 money managers, and 1,204 community investment institutions that practice “ESG incorporation” by applying ESG criteria in their investment analysis and portfolio selection.2

The “duration tailwind” that began with the Paul Volcker Federal Reserve (Fed) of the early 1980s was in full swing by the early 2000s (Phase 1), helping the rock stars of fixed income add alpha relative to the Agg and zeros to their bank accounts. Most investors at the time did not believe another 20+ years of duration tailwind was to come (Phase 2), which ultimately proved to be the right call. Thrill-seeking contrarians like Jim Grant from Grant’s Interest Rate Observer, pleaded for higher rates time, and again, only to remain befuddled by still-lower rates and below-trend growth.

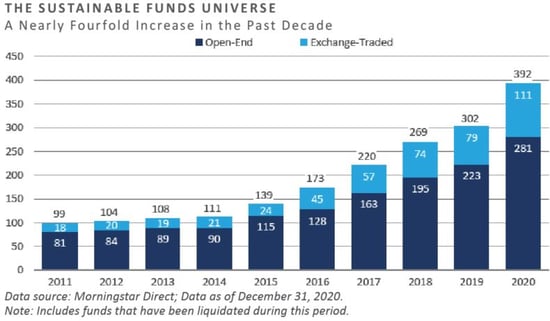

GROWTH IN INVESTMENT OPTIONS

FEG has also witnessed significant growth in the investment options available to align investor’s portfolios with their values, ranging from exchange-traded and mutual funds, to customized direct index and separately managed accounts, to a wide variety of private funds. In 2020, 71 sustainable mutual funds/ETFs were launched, easily topping the previous high-water mark of 44 set in 2017.3

In addition to the abundance of investment options, the amount allocated to sustainable funds has also greatly increased. Sustainable funds attracted a record $51.1 billion in net flows in 2020—more than double the previous record set in 2019. In that same year, sustainable fund flows accounted for nearly a fourth of overall flows into funds in the U.S.4

BEWARE OF GREENWASHING

As more individual and institutional investors express interest in Responsive Investing, some funds have changed their name in an effort to capture investor interest. The term “greenwashing” suggests the change in name is superficial and that the funds did not also change their investments. Just two years ago, it was uncommon to find any reference to ESG in the offering documents of traditional funds. Now, however, many funds indicate in their prospectuses that they may consider ESG factors at some point in their investment process.6

To avoid potential greenwashing it is paramount for an investor to understand a fund’s true alignment with their values. To that end, we screen potential managers through our Six Tenet Manager review process in an effort to understand their intentionality.

An institutional approach

Institutional investors have also increased the amount of assets devoted to ESG. According to the US SIF Foundation’s 2020 report, public funds represent the largest number of assets and institutions reporting ESG criteria (54%), followed by insurance (36%), education (6%), and foundations (2%).7

The report ranks the top criteria considered by institutional investors. Overall, the top concern was conflict risk, followed closely by climate change.

However, the importance of each factor varies based on segment. The segment and top leading criteria are as follows:

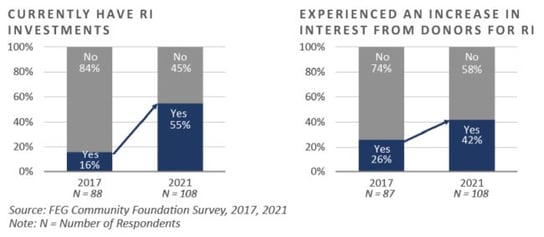

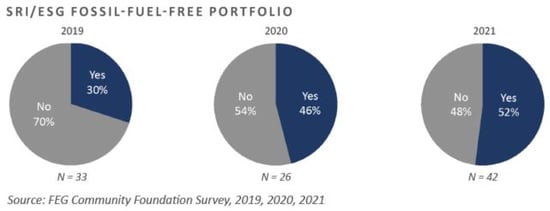

RESPONSIVE INVESTING IS ALSO A GROWING TREND WITHIN COMMUNITY FOUNDATIONS

Based on FEG’s proprietary community foundation survey, we have also seen increased interest in Responsive Investing. The 2021 FEG Community Foundation Survey saw the number of respondents with some allocation to Responsive Investing surpass 50% for the first time, although the dollar amount was limited.

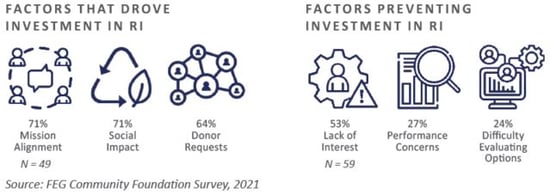

The factors driving investment were much more consistent, with more than 70% of respondents agreeing that mission alignment and having a social impact led community foundations to investing in RI. Factors preventing a responsive investment were not as consistent, though approximately 50% cited a lack of interest in Responsive Investing.

Additionally, the survey saw an increase in participants with fossil fuel free portfolios, crossing the 50% threshold for the first time.

ways to allign values and investments

The process of aligning an investor’s mission with their investments is more than just a single decision, it is often a journey to determine the suitable implementation strategy. It can also be an evolution that starts with one approach and adopts others over time.

Some of the most common approaches for aligning values and an investment portfolio include:

Negative Screening/Divestment

Negative screening is the most commonly used approach by investors focused on being socially responsible. This approach calls for the exclusion of companies or industries an investor might consider morally unsuitable given their unique mission and values. Negative screens are also often used as a means to enact political and social change. For example, divestment played a role in investors choosing to seek social changes such as fighting apartheid in South Africa, going “tobacco free,” promoting “no sin stock” investing, and, more recently—particularly of topic for some universities, driven by student activism—“fossil fuel free” investing.

Impact Investments

Impact investments are made with the intention to generate positive, measurable social and environmental impact. Impact investments can be made in both emerging and developed markets, and target a range of returns from below market to market rate, depending on an investor’s strategic goals. Examples include affordable housing and micro-finance for underserved communities.

Program-Related Investing (PRI)

A PRI is an investment (e.g., loan, equity investment, or financial guaranty) made by a foundation to pursue its charitable mission rather than to generate income. The recipient can be a nonprofit organization or a for-profit enterprise. PRIs originated as part of the U.S. Tax Reform Act of 1969.

Sustainable Investing

Sustainable investing can be described as an investment discipline that directs investment capital to companies which seek to promote corporate responsibility and natural resource sustainability. A primary example of this type of investment is renewable energy.

Investor/Shareholder Advocacy

Another way investors can encourage companies to change is through proxy voting and by sending letters and filing proposals to engage in dialogue. Not surprisingly, there are groups of investors that have effectively promoted changes to companies.

Community Investing

The community investing sector has experienced rapid growth over the last decade. Community investing assets nearly doubled between 2014 and 2016, increased another 50% between 2016 and 2018, and most recently grew 44% between 2018 and 2020. Today there over 1,200 community development financial institutions at work across all 50 states.8 Examples include:

- Community Development Banks – For-profit institutions that focus on providing capital to economically distressed communities, primarily through targeted lending and investing. They typically have community members on their board and deposits are FDIC insured.

- Community Development Credit Unions – Nonprofit financial cooperatives owned by members. In terms of asset weight, they constitute the largest group of community investing institutions. Deposits in community development credit unions are generally NCUA insured. Assets among credit unions have grown 49% since 2018 to more than $180 billion.

- Community Development Loan Funds – Tend to be nonprofit organizations which provide financing and development services to businesses, organizations, and individuals in low-income communities. This is the most common type of community investing institution, with nearly 600 community loan funds and $27 billion in combined assets as of 2020.

- Community Development Venture Capital – A type of private equity investment targeted at financially underserved low- and moderate-income communities. Assets in these funds have increased by 57% since 2018, to more than $370 million in 2020, although their numbers and assets remain among the smallest segment of community investing institutions.

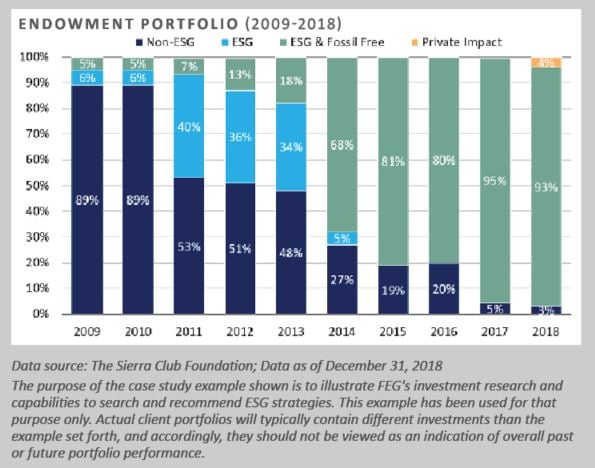

A case studyprogress towards mission alignmentAs an example of aligning mission and investments, this foundation went from having an interest in Responsive Investing to winning an industry award by CIO Magazine for “ESG Innovator of the Year” within a decade. The foundation started with negative screening and eventually moved to divestment. Later, they began investing in impact solutions, utilizing shareholder engagement, which grew to include private impact investments.

While this is the path of one client, each organization is unique and can start with any approach. The decision on which approach to use depends on the needs of the specific client and can be facilitated through a discovery process. |

Are There Industry Guidelines for Responsive Investing?

There are numerous groups focused on building frameworks to promote and standardize corporate reporting, disclosure, and transparency. Each develop their own guidelines—typically with a specific focus. A few of the largest include:

Principles for Responsible Investment (PRI)

FEG is a proud signatory of PRI, the world’s leading initiative on responsible investment, which was founded in 2006. To learn more about FEG’s involvement, please read our announcement.

Members of the organization work to better understand the investment implications of ESG factors in accordance with PRI’s six principles for responsible investment. The principles are a voluntary and aspirational set of investment guidelines that offer a menu of possible actions for incorporating ESG issues into investment practice.

PRINCIPLE 1: We will incorporate ESG issues into investment analysis and decision-making processes.

PRINCIPLE 2: We will be active owners and incorporate ESG issues into our ownership policies and practices.

PRINCIPLE 3: We will seek appropriate disclosure on ESG issues by the entities in which we invest.

PRINCIPLE 4: We will promote acceptance and implementation of the Principles within the investment industry.

PRINCIPLE 5: We will work together to enhance our effectiveness in implementing the Principles.

PRINCIPLE 6: We will each report on our activities and progress towards implementing the Principles.

The PRI initiative provides research and education to help investors align their responsible investment practices with the broader objective of a more sustainable society as defined by the Sustainable Development Goals (SDGs). Many organizations also select specific SDG goals that align with their mission. For example a community foundation client may opt to focus on SDGs 1, 2, and 5, while a healthcare nonprofit may focus on SDG 3.

Global Reporting Initiative (GRI)

This initiative was established in 1997 to create an accountability framework for companies to display their responsible environmental business practices to stakeholders. The recently revised (2021) Universal Standards represent the most significant update since GRI transitioned from providing guidance to setting standards in 2016. The GRI Standards allow an organization to report information in a way to cover all of its most significant impacts on the economy, environment, and people, or to focus only on specific topics, such as climate change or child labor.

Carbon Disclosure Project (CDP)

CDP is a nonprofit founded in 2000 that runs a global disclosure system to help investors, companies, cities, states, and regions manage their environmental impact.

Climate Disclosure Standards Board (CDSB)

CDSB was formed at the annual meeting of the World Economic Forum in 2007. The CDSB is an international consortium of business and environmental NGOs (Non-Governmental Organizations) committed to advancing and aligning the global mainstream corporate reporting model to equate natural capital with financial capital by offering companies a framework for reporting environmental information to assess risks and opportunities. In light of changing market demands, the CDSB framework was last refined in 2019.Sustainability Accounting Standards Board (SASB)

In 2011, the SASB began developing standards to indicate both sustainability and strong financial fundamentals. SASB’s standards guide companies’ disclosure of financially material sustainability information to their investors. Available for 77 industries, the standards identify the subset of ESG issues most relevant to financial performance in each industry.

Taskforce on Climate-Related Financial Disclosures (TCFD)

G20 finance ministers and central bank governors asked the Financial Stability Board (FSB) to review how the financial sector can take account of climate-related issues. The FSB established the TCFD in 2015 to develop recommendations for more effective climate-related disclosures that could promote more informed investment, credit, and insurance underwriting decisions and, in turn, enable stakeholders to understand better the concentrations of carbon-related assets in the financial sector and the financial system’s exposures to climate-related risks. In 2017, the TCFD released climate-related financial disclosure recommendations designed to help companies provide better information to support informed capital allocation.

United States Conference for Catholic Bishops (USCCB) Principles for Investments

The USCCB is called to exercise faithful, competent, socially responsible stewardship in managing its financial resources. As a Catholic organization, the conference draws its values and the directions and criteria to guide its financial choices from the gospel, universal church teaching, and USCCB statements. The combination of religious mandate and fiscal responsibilities suggests the need for a clear and comprehensive set of policies to guide the USCCB's investments and other activities related to corporate responsibility. Originally provided in 2003, the USCCB guidelines were updated in November 2021. Learn more about these updates here.

Workforce Disclosure Initiative (WDI)

WDI was created in 2016 by the UK nonprofit ShareAction. The framework, modeled after the CDP, collects data on the management of both direct employees and supply chain workers in an effort to provide institutional investors with meaningful information. WDI aims to improve corporate transparency and accountability on workforce issues, provide companies and investors with comprehensive and comparable data, and help increase the provision of good jobs worldwide.

The Evolution of Data — Measuring Alignment With Values

Driven by the tremendous growth in interest and assets, one of the challenges facing investors is inconsistent data standards and measurement across the industry. Consequently, numerous rating agencies have developed their own approach to

collecting data and providing output. By some counts, there are over 100 such groups seeking to provide a framework for measurement and ranking the data for Responsive Investing. As investors consider reporting on their assets, it is important to understand the various groups engaged in promoting better standards and improved transparency.

Investors should understand that inconsistent data isn’t necessarily surprising given the growth of Responsive Investing and the sheer number of parties involved; each promoting their own views, approaches, and evolving standards. Investors can take some comfort in simply knowing that data and frameworks are encouraging more corporate disclosures.

While there are a number of ESG rating companies, here are some of the most prominent ones:

Bloomberg ESG Data – Bloomberg’s Environmental, Social & Governance dataset offers ESG metrics and ESG disclosure scores. They include data as-reported by companies, as well as sector- and country-specific data.

Fitch Ratings ESG Relevance Scores Data – Fitch Solutions provides insights, tools, and data in an effort to help bring clarity to the ESG financial community.

ISS Environmental and Social Quality Score – This rating company features a data-driven scoring and screening solution designed to measure and identify areas of environmental and social risk through company disclosure. They focus on environmental and social areas of concern.

Moody’s ESG – Sustainability and climate change are fundamental considerations for those investors looking to seize opportunities and manage risk in today’s global capital markets. Moody’s data and insights cross ESG factors and climate risks, as well as sustainable finance.

MSCI – MSCI has an ESG Rating that measures a company’s resilience to long-term, industry material ESG risks. MSCI uses a rules-based methodology to identify industry leaders and laggards according to their exposure to ESG risks and how well they manage those risks relative to peers. The MSCI ESG Ratings span from leader (AAA, AA), to average (A, BBB, BB), to laggard

(B, CCC). MSCI also rates equity and fixed income securities, loans, mutual funds, ETFs, and countries.

S&P Global Ratings –The S&P Global Ratings ESG Evaluation provides an assessment of a company’s ESG strategy and ability to prepare for potential future risks and opportunities. The methodology is founded on analysts’ sector and company expertise, relying upon in-depth engagement with company management to assess material ESG impacts on the company—past, present, and future.

Refinitiv – Refinitiv’s ESG scores measure a company's relative ESG performance, commitment, and effectiveness across 10 main themes, based on publicly available and auditable data.

Sustainalytics – Sustainalytics’ ESG Risk Ratings are designed to help investors identify and understand financially material ESG risks at the security and portfolio level and how they might affect the long-term performance for equity and fixed income investments.

Ultimately the data provided by these companies should help investors answer some of the following questions:

- How aligned are our investments and our mission?

- Which factors are financially material to our mission?

- How effective is our stewardship?

- Can we communicate the impact of our invested capital?

- Is this approach delivering long-term value creation?

- How are we contributing to a better society and economy?

Conclusion

Responsive Investing has experienced explosive growth over the past several years, and we believe this growth will continue. It is an exciting time for those interested in aligning their investments with their values. Importantly, FEG believes investors do not necessarily have to sacrifice returns to achieve alignment with values.

As organizations consider Responsive Investing, it is important to identify the core values and approach that best suits the organization today, while understanding what framework and data measurement can best serve the organization’s needs going forward.

At FEG, our goal is to help clients achieve excellence as stewards of their investment assets. With decades of experience assisting investors in various stages of Responsive Investing—from those taking their initial steps to those seeking full alignment and impact measurement—FEG has the experience and track record to help investors of all types determine a strategy that is in line with their values and goals. Regardless of the level of implementation, we can facilitate a discovery process to determine an investor’s priorities and develop a suitable approach for the organization.

Contact us

We look forward to sharing our ideas and solutions with you. For more details on Responsive Investing, please contact us.

resources

Center for Sustainable Finance & Private Wealth – Unleashing the Potential of Faith-Based Investors for Positive Impact and Sustainable Development

Georgeson – The ABCs of ESG: Initiatives and Organizations Issuers Should Understand

Global Impact Investing Network (GIIN) – Annual Impact Investor Survey 2020

Global Sustainable Investment Alliance (GSIA)

Morningstar Manager Research – Sustainable Funds U.S. Landscape Report 2020

NonProfit Quarterly – Trouble in Paradigm: Foundations' Bargain with the Devil, June 2021, Clara Miller

Organisation for Economic Co-operation and Development (OECD)

The SustainAbility Institute – Rate the Raters, 2020

US SIF Foundation – Report on US Sustainable and Impact Investing Trends, 2020

FOOTNOTES

3, 4, 5, 6 Morningstar, Sustainable Funds U.S. Landscape Report, 2020

DISCLOSURES

Responsive Investing (RI) and all aspects of our services related to RI are done by FEG on a best-efforts basis. Because of various limitations due to the very nature of the various ESG issues, FEG cannot guarantee that RI will align with or achieve the expected ESG values or investment returns. Further, FEG relies on third-party service providers to determine whether various investments meet the applicable ESG characterizations, and FEG's ability to correctly categorize the ESG exposures of the investments will depend in large part on the accuracy of the third-party service providers. There can be no assurance that the third-party service providers will correctly characterize the investments. Additionally, in many cases, FEG relies on representations from its investment managers and may not have the ability to verify the accuracy of the representations due to limited transparency.

This report was prepared by Fund Evaluation Group, LLC (FEG), a federally registered investment adviser under the Investment Advisers Act of 1940, as amended, providing non-discretionary and discretionary investment advice to its clients on an individual basis. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser.

The information herein was obtained from various sources. FEG does not guarantee the accuracy or completeness of such information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. FEG assumes no obligation to update this information, or to advise on further developments relating to it.

Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell any securities.

Any return expectations provided are not intended as, and must not be regarded as, a representation, warranty or predication that the investment will achieve any particular rate of return over any particular time period or that investors will not incur losses.

Past performance is not indicative of future results.

This report is prepared for informational purposes only. It does not address specific investment objectives, or the financial situation and the particular needs of any person who may receive this report.

Fund Evaluation Group, LLC, Form ADV Part 2A & 2B can be obtained by written request directed to: Fund Evaluation Group, LLC, 201 East Fifth Street, Suite 1600, Cincinnati, OH 45202 Attention: Compliance Department.

Published February 2022