-01.webp?width=400)

In Brief

- Market conditions are increasingly defined by dispersion across company fundamentals, valuations, sectors, and global economies, creating a wider range of outcomes that can favor hedge fund strategies.

- Hedge funds can capitalize on valuation gaps, corporate events, and policy divergence—sources of return that are less dependent on broad market direction.

- For institutional portfolios, hedge funds may serve as a complement to traditional diversification, particularly in environments where equity and bond correlations rise and macro uncertainty persists.

Diversification Under Pressure

Periods of market stress often reveal the strengths and limitations of traditional portfolio construction.

In 2022, both equities and bonds declined meaningfully as inflation surged and central banks tightened policy. The S&P 500 Index and global equities as a whole (MSCI ACWI) both declined by over 18%, while the Bloomberg Barclays Aggregate Bond Index lost 13%. For many institutional portfolios, the simultaneous drawdown across asset classes highlighted the challenge of relying on traditional diversification alone during inflationary and policy-driven shocks.

Hedge funds, while not immune to market volatility, exhibited a different pattern of returns. Performance varied across strategies, but outcomes were generally more dispersed. Event-driven strategies declined almost 5%, equity hedge strategies fell just over 10%, and relative value strategies were nearly flat. Macro strategies, in contrast, generated positive returns of 9%, benefiting from volatility across rates, currencies, and commodities.

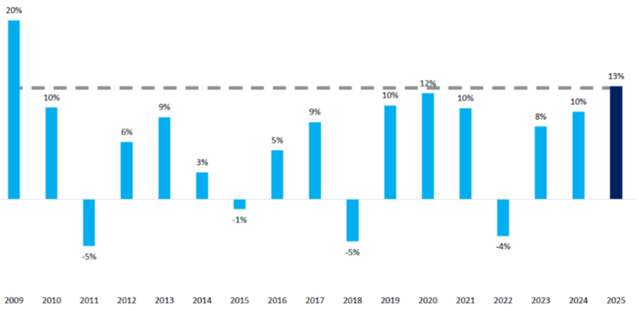

Hedge Funds to Post the Best Calendar-Year Returns in 16 Years

Data Source: FEG, HedgeFund Research

Data as of December 31, 2025.

This dispersion of outcomes within hedge fund strategies translated into more resilient aggregate results relative to traditional markets. More importantly, it demonstrated the value of return streams that are not solely dependent on market direction.

For institutional investors, the takeaway was not that traditional diversification is ineffective, but that it may be incomplete in certain environments—particularly those characterized by inflation shocks, policy shifts, or elevated correlations across risk assets.

From Concentration to Dispersion

The hedge fund opportunity set is expanding in a market increasingly defined by dispersion rather than concentrated rallies in traditional risk assets. In recent years, correlations across traditional asset classes have remained elevated, while policy uncertainty and structural economic shifts have contributed to higher volatility across markets. In this environment, additional differentiated return streams can provide a more reliable source of diversification than traditional asset exposures alone.

Periods of wide valuation gaps, elevated earnings dispersion, higher interest rates, and frequent factor rotations tend to create fertile ground for hedge fund strategies. Unlike long-only portfolios that rely primarily on market direction, hedge funds can capitalize on relative mispricings and company or economic changes.

Fundamental Long/Short: Opportunities in Valuation and Balance Sheets

Fundamental long/short strategies—across both equities and credit—are particularly well positioned in today’s environment characterized by widening dispersion. Several forces, including higher financing costs and the rapid integration of new technologies, are driving these divergences.

Higher interest rates, in particular, are reshaping corporate balance sheets and increasing the importance of capital structure discipline. Companies that relied on low-cost financing during the previous decade are now facing refinancing challenges, while firms with strong balance sheets and durable cash flows are gaining competitive advantages. This dynamic creates opportunities for managers to identify both long and short positions based on balance sheet resilience and earnings durability.

The evolution of artificial intelligence (AI) also illustrates how structural technological change can drive dispersion. Companies successfully integrating AI into their business models may experience meaningful productivity gains and margin expansion, while others may struggle to adapt. At the same time, the substantial capital required to build AI infrastructure—from data centers to specialized hardware—has created additional financing needs. Convertible securities, often used to fund high-growth technology initiatives, experienced explosive issuance in 2025—hitting a 24-year high of $167 billion last year. This is one example of how the AI investment cycle may expand opportunities across both equity and credit long/short strategies.

Event-Driven: Corporate Evolution and Structural Change

Event-driven strategies, including merger arbitrage and distressed investing, may also benefit from the evolving corporate landscape.

Merger arbitrage opportunities often increase when regulatory environments shift or when strategic consolidation accelerates. In recent years, regulatory scrutiny has slowed the pace of mergers and acquisitions, widening spreads for arbitrage investors. However, as regulatory conditions evolve and corporations pursue strategic combinations to remain competitive, deal activity has been increasing. The technological transformation driven by AI may also create new synergies that encourage consolidation across industries such as semiconductors, software, and infrastructure.

Distressed investing may see a similarly expanding opportunity set. Higher interest rates, tighter credit conditions, and shifting competitive dynamics are placing pressure on highly leveraged firms. Companies unable to adapt to technological disruption or rising financing costs may be forced to restructure their balance sheets or exit the market altogether. These situations can create attractive entry points for investors specializing in restructurings, special situations, and capital structure arbitrage.

Macro and Relative Value: Volatility Across Global Markets

Macro and relative value strategies are well-suited to an environment characterized by diverging central bank policies and shifting global economic conditions. These forces can generate significant volatility both between and within asset classes.

Central banks around the world are navigating different inflation dynamics and growth trajectories. As a result, interest rate paths across Japan, the Bank of England, the European Union, and the U.S. are increasingly divergent. Currency, commodity, and global rate markets often respond sharply to these policy differences, creating opportunities for macro-oriented investors.

Recent moves in the U.S. dollar and gold illustrate how macroeconomic narratives can drive outsized price movements across assets. Global macro and relative value managers can capitalize on these dislocations by identifying both short-term volatility and longer-term trends across currencies, rates, and commodities.

The Portfolio Role of Hedge Funds

More important for investors than the opportunities within individual strategies, hedge funds play an important diversifying role at the portfolio level. By nature, institutional portfolios are heavily dominated by equity risk, even when diversified across public and private markets, because of their long investment horizon and total return goals. During periods of market stress, however, portfolios are not immune to meaningful drawdowns and increased portfolio volatility.

Hedge funds can offer several benefits in this context. Many strategies have moderate to low correlation with traditional risk assets such as equities and bonds, allowing them to act as diversifying return streams. Additionally, hedge funds often emphasize capital preservation and opportunistic positioning, which can help mitigate drawdowns during periods of market turbulence. In inflationary environments, when equity and bond correlations can rise—hedge funds may provide a more effective source of diversification.

By combining differentiated sources of return with lower directional market exposure, hedge funds can enhance overall portfolio efficiency. In many cases, they can improve risk-adjusted returns while dampening volatility, particularly during environments when traditional diversification benefits weaken.

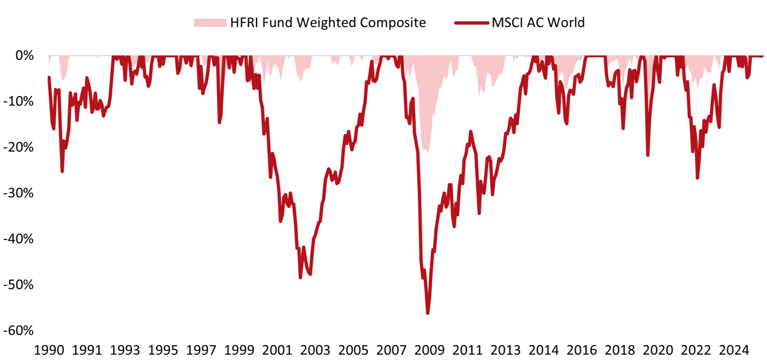

Capital Preservation Profile

Hedge Funds Performance During Global Equities Drawdowns (Displaying Negative Returns Only)

Data Source: HedgeFund Research, MSCI, FactSeta

Data as of December 31, 2025.

Positioning for a More Dispersed Market

Market conditions characterized by greater dispersion across companies, sectors, and economies can challenge traditional long-only portfolios. At the same time, they tend to expand the opportunity set for hedge fund strategies.

We believe fundamental long/short managers can benefit from valuation and balance-sheet dispersion, event-driven investors can capitalize on corporate restructuring and consolidation, and macro and relative-value strategies can benefit from global policy divergence, market volatility, and price dislocations. Combined with their potential to reduce portfolio drawdowns and improve diversification, hedge funds may play an increasingly valuable role in institutional portfolios as market dynamics continue to evolve.

DISCLOSURES

This information was prepared by Fund Evaluation Group, LLC (FEG), a federally registered investment adviser under the Investment Advisers Act of 1940, as amended, providing non-discretionary and discretionary investment advice to its clients on an individual basis. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Fund Evaluation Group, LLC, Form ADV Part 2A & 2B can be obtained by written request directed to: Fund Evaluation Group, LLC, 201 East Fifth Street, Suite 1600, Cincinnati, OH 45202 Attention: Compliance Department.

This information is prepared for informational purposes only. It does not address specific investment objectives, or the financial situation and the particular needs of any person who may receive this presentation. Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell any securities.

The information herein was obtained from various sources. FEG does not guarantee the accuracy or completeness of such information provided by third parties. The information in this presentation is given as of the date indicated and believed to be reliable. FEG assumes no obligation to update this information, or to advise on further developments relating to it.