-01.webp?width=400)

Over the past few days, the United States and Israel have conducted coordinated military operations targeting Iranian leadership and strategic assets. The geopolitical significance is evident, and headlines have been dramatic. Markets, however, tend to look past the headlines and focus on a narrower question: does the event meaningfully alter the trajectory of economic activity or financial conditions?

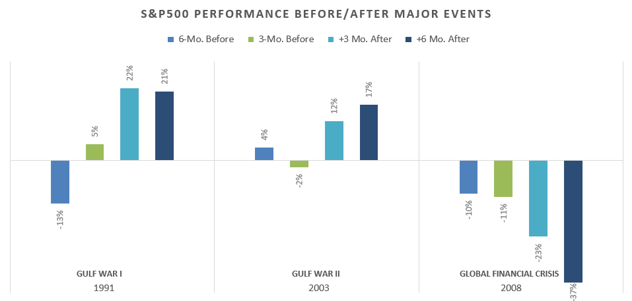

History suggests that most geopolitical events, while newsworthy, typically do not occur in centers of economic activity and therefore tend to have limited, often short-lived, impacts on financial markets. Consider the beginning of the two Gulf Wars versus the 2008 global financial crisis (GFC). Markets experienced volatility around those events but generally stabilized in the months that followed. The key difference was that those conflicts did not disrupt the underlying financial system, unlike the systemic crisis of the GFC.

Data Source: Strategas Research Partners

In this case, the most direct market impact would likely come through energy.

Why This Event Matters for Energy Markets

Iran remains an important, if not dominant, player in the global oil market. As of early 2026, it produces approximately 3.2 to 3.4 million barrels of crude oil per day, accounting for roughly 3% to 4.5% of global supply and ranking it among OPEC’s larger producers. Despite international sanctions, Iran has sustained this output, with exports estimated at around 1–2 million barrels per day, primarily to China and other parts of Asia.

While Iran’s production is smaller than that of Saudi Arabia and Iraq, the broader Gulf region remains substantial for global energy flows. Approximately 20% of the world’s oil passes through the Strait of Hormuz, a narrow chokepoint between Oman and Iran that is essential to global energy trade. That makes it one of the most important chokepoints in the global economy. Oil is not the only portion of the energy market affected. On March 2, Qatar halted liquified natural gas (LNG) production after intercepting Iranian drones. Because energy is a fundamental input into transportation, industry, and consumer goods, changes in its price feed through to inflation, corporate margins, and broad financial conditions.

Transmission to Inflation and Markets

When geopolitical risk intersects with energy infrastructure or key supply chains, economic transmission becomes clearer:

-

Oil and energy prices move first. Even the threat of disruptions in the Strait of Hormuz can introduce a geopolitical risk premium into crude markets, and traffic through the waterway dwindled to almost nothing following the joint operations. Recent spikes in Brent and WTI prices reflect this risk pricing.

-

Inflation expectations adjust. Higher energy costs tend to raise headline inflation and can complicate central bank policy decisions.

-

Financial conditions tighten. If higher energy prices persist, they can begin to feel like a tax on consumers and businesses, reducing discretionary spending and pressuring margins.

In short, oil and its downstream effects are at the center of this market reaction.

Oil, Inflation, and Policy Implications

The macroeconomic risk is straightforward:

-

A sustained spike in crude prices would lift headline inflation.

-

Higher inflation could complicate central bank policy.

-

Elevated energy costs would weigh disproportionately on lower-income consumers and energy-intensive sectors.

That said, energy markets have historically adjusted through a combination of strategic petroleum reserve releases, rerouted shipping, production responses from OPEC and U.S. shale, and demand elasticity at higher price levels.

The key variable is duration. Short-lived supply fears tend to fade. Prolonged shipping disruptions through the Strait of Hormuz would be more consequential.

Bottom Line

The macroeconomic risk is straightforward:

Geopolitical events are inherently unpredictable and emotionally charged. Markets, however, ultimately tend to respond less to headlines and more to underlying economic fundamentals. In this case, those fundamentals are in the energy markets.

If energy flows remain largely intact and price spikes prove temporary, the market impact is likely to resemble prior geopolitical episodes: volatility, headline-driven swings, and eventual stabilization.

If the conflict materially disrupts oil supply or shipping through the Strait of Hormuz for an extended period, the inflationary consequences could become more persistent, with broader implications for growth and monetary policy.

For now, this development adds to an already long list of uncertainties confronting investors — trade policy shifts, fiscal dynamics, monetary policy transitions, the implications of the AI build out, and evolving global growth trends. It does not, at this stage, appear to meaningfully alter the underlying structure of the U.S. economy or financial system.

DISCLOSURES

This information was prepared by Fund Evaluation Group, LLC (FEG), a federally registered investment adviser under the Investment Advisers Act of 1940, as amended, providing non-discretionary and discretionary investment advice to its clients on an individual basis. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Fund Evaluation Group, LLC, Form ADV Part 2A & 2B can be obtained by written request directed to: Fund Evaluation Group, LLC, 201 East Fifth Street, Suite 1600, Cincinnati, OH 45202 Attention: Compliance Department.

This information is prepared for informational purposes only. It does not address specific investment objectives, or the financial situation and the particular needs of any person who may receive this presentation. Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell any securities.

The information herein was obtained from various sources. FEG does not guarantee the accuracy or completeness of such information provided by third parties. The information in this presentation is given as of the date indicated and believed to be reliable. FEG assumes no obligation to update this information, or to advise on further developments relating to it.