-01.webp?width=400)

In early April 2024, astronomy enthusiasts—including several FEG team members—flocked to the path of totality to observe the solar eclipse. Although the moon is 400 times smaller than the sun, it completely obscured the sun for over four minutes. Not only was the solar phenomenon fascinating to observe, but also the varied behaviors of animals—for example, manic birds—and reactions from viewers ranging from tearful to “meh.” For many, it was a once-in-a-lifetime event. Some, however, who had viewed the relatively recent solar eclipse of 2017, sported t-shirts that read “Twice in a Lifetime."

TOTAL ECLIPSE — TWICE IN A LIFETIME?

A PREVIEW OF 2024 NACUBO RESULTS

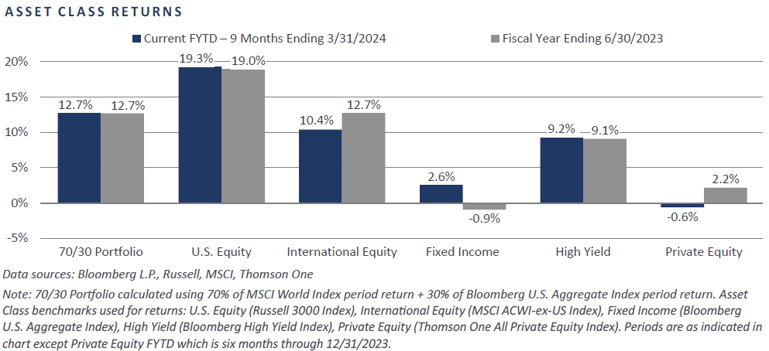

Investors may be experiencing a similarly rare repeat. Most higher education institutions have a fiscal year ending 6/30/2024. Comparing the first nine months of the current fiscal year (through 3/31/2024) versus the previous full fiscal year (ending 6/30/2023) for illustrative trends, major asset classes are on track to deliver remarkably similar returns to the prior fiscal year. In fact, a 70/30 portfolio for each of these periods returned 12.7%, and many underlying asset classes are comparably aligned over the two periods. For example, U.S. large-cap growth equity has continued to dominate all other asset classes, yet private equity is lagging public equity significantly—a rare phenomenon in any year, let alone over two consecutive years. If fiscal 2024 endowment portfolio returns finish close to where they are tracking (admittedly a big “if”), then higher education endowments with large allocations to alternative investments may underperform peers with more liquid allocations for the second year running.

Such periods of volatility can lead to many questions about the implications of these trends. Will private equity and hedge funds ever shine again, or will other asset classes continue to eclipse returns? Should educational institutions alter portfolio construction or spending to navigate budgets and liquidity concerns? This insight piece will examine these questions and explore how investment committee members can best communicate to donors and university constituents during periods of uncertainty, delving into past trends, current questions facing college and university investment committees and boards, and projections for long-term positioning.

FEG has been advising higher education institutions for over 35 years, and supports organizations by providing detailed spending and liquidity analyses, stress testing portfolio construction, educating on best governance practices among peers, and curating communication plans for boards and other university constituents. We believe each institution’s asset allocation and investment approach should be aligned with their unique objectives, risk tolerance, and principles. It is therefore important that each institution take into account the level of operating budget covered by their endowment, anticipated changes in tuition and enrollment, amount of support from gifts and state entities, and rising costs.

PAST TRENDS

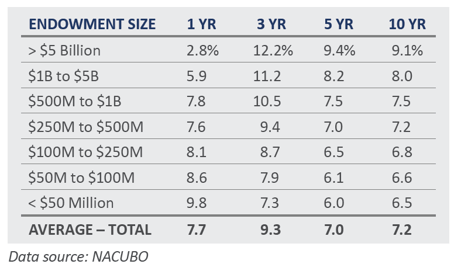

June 30, 2023, marked the 50th anniversary of the National Association of College and University Business Officers’ (NACUBO) annual study of college and university endowments and related foundations. The study provides an analysis of endowment investment returns, asset allocations, and governance policies. The past 35 years saw the evolution of the “endowment model” which leans heavily into equity and alternative assets. Institutions that adopted higher allocations to illiquid strategies, such as private equity, debt, real estate, and real assets, have certainly benefited. The 2023 NACUBO survey indicates that the largest institutions (> $5 billion) which held an average 63% allocation to alternative strategies—private capital plus hedge funds—returned 9.1% annualized over 10 years net of manager fees. This is a 2.6% premium relative to the smallest cohort (< $50 million), which held about 10% in alternatives on average. That return premium was 4.9% over three years and 3.4% for five years.

NACUBO results for 2023—potentially to be repeated in 2024—upended the status quo when private capital allocations were a drag on performance, leading smaller institutions to outperform their larger counterparts materially. The <$50m cohort saw returns of 9.8%, beating the largest institutions by a full 7.0%. Some institutions with heavy venture capital allocations even reported negative fiscal year results.

Over the past decade, allocations to low yielding fixed income and hedge funds did not keep pace with riskier assets. Low interest rates magnified the valuation multiples for public equity, propped private equity investments with easy access to capital, and revived real estate with low cap rates. This culminated in a stellar fiscal year 2021 for private equity, with the Thomson One All Private Equity Index climbing 64%. When the 70/30 public portfolio subsequently declined 13% in fiscal year 2022, some investors suddenly found themselves overallocated to private capital while at the same time facing budget and liquidity concerns due to higher inflation costs.

Committee and board members, in their fiduciary oversight role, should understand the long-term strategy and the short-term drivers of their endowment portfolios as they often represent their institutions to donors, university constituents, and the public.

CURRENT TRENDS

As indicated previously, institutions are increasingly fielding questions about endowment portfolio construction and performance, which has heightened focus on spending and liquidity.

When markets are changing rapidly, there is a temptation to appear responsive by making inevitably mistimed portfolio changes. An institution’s focus should rather be on good communication, not on changing the portfolio to meet shifting market trends. Institutions should develop an asset allocation strategy that will enable the organization to thrive through cycles with various market environments. Portfolios must also be stress tested to ensure they are within appropriate liquidity and risk guidelines in a worst-case scenario. And the justification for such prudence is clear: during the past few years, investors have experienced three full bear market declines—a 20% drop from peak in the S&P 500—including a global pandemic, several geopolitical crises, and rampant inflation.

During periods of market volatility, questions from constituencies can become opportunities for committee and board members to champion the endowment. To achieve this, they should be equipped with simple talking points that explain the following:

- We understand the primary drivers of the markets and portfolio (e.g., performance attribution, private capital j-curve).

- We have a long-term investment strategy that anticipates market volatility.

- We have stress-tested the portfolio for such periods and are within appropriate liquidity and risk guidelines.

- We are proactively embracing opportunities caused by distress rather than reacting defensively or chasing recent rallies.

Portfolio returns are intended to support consistent spending distributions; so when portfolio growth is in question, it is natural for institutions to revisit spending policies. Many institutions are facing budget challenges, either from slowing revenue, increasing expenses, or both. This has led some to consider a change in their spending rate and calculation methodology, or at a minimum to forecast scenarios for budget planning. Similarly, institutions are concerned about the impact on year-to-year spending distributions caused by market value fluctuations. Complicating things further, many endowment market values peaked at fiscal year end June 30, 2021, elevating spending draws for those with rolling average calculations for several years.

Institutions have considered several options: increasing the number of rolling periods to smooth returns, reducing the spending percentage rate gradually, and adopting hybrid spending methods to limit spikes or craters in draws. Institutions facing operating deficits often explore increasing spending temporarily or taking one-off distributions to cover operating deficits, or even leveraging the portfolio for loans. Stress testing these scenarios for potential market declines can be a useful planning tool.

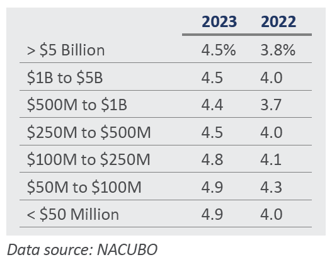

The 2023 NACUBO survey indicates a recent rise in effective spending, caused in part by changes in portfolio market values.

Liquidity analysis becomes increasingly important as an institution’s private capital allocation increases, as funds must be readily accessible to meet irregular capital calls. Flat or declining public equity markets can also strain liquidity resources for institutions that must withdraw from the portfolio each year. Gifts and the level of draws needed for university operations should also be considered. Fortunately, higher yields on cash and fixed income means that these liquidity assets are no longer the headwind that they were when rates were near zero. Higher interest rates also present creative opportunities for operating cash management.

Taking all these factors into account, we believe institutions should determine their minimum required liquidity and repeat stress testing. Liquidity should be viewed not only as a minimum level of protected assets that is readily accessible, but also as an asset which can be deployed for alpha during periods of distress when others in need of liquidity would be forced to sell long-term assets.

PROJECTED TRENDS

Despite current economic, market, and political uncertainty, markets are generally sitting at reasonable levels. In part, this is evidenced by mixed economic indicators that support arguments for both a strengthening and a weakening economy. Although there are some areas of concern—such as elevated U.S. equity valuations—earnings growth is increasing and interest rates are very near historical averages.

In this environment, FEG recommends staying close to strategic targets until more obvious areas of opportunity or risk emerge. Private capital should continue to deliver premium returns from its vast and inefficient opportunity set. As always, however, implementation must be dynamic—and good manager selection remains vital. Fixed income will play a more important role with higher yields. FEG’s investment team remains cautious in real estate and hedge funds, as interest rates provide a higher hurdle for these asset classes to deliver excess return.

CONCLUSION

While the current NACUBO trends appear to have cast a shadow on the endowment model’s success, FEG expects this eclipse to be temporary and advises investors to stick to their institution’s strategic plan, re-underwrite spending and liquidity needs, and continue to allocate to private capital. The drivers of portfolio performance will continue to be long-term strategic asset allocation and diversification, although there will also inevitably be dislocations which provide opportunities for patient investors to tilt their portfolios toward additional alpha opportunities. FEG’s advisory team stands ready to assist colleges and universities.

DISCLOSURES

This report was prepared by FEG (also known as Fund Evaluation Group, LLC), a federally registered investment adviser under the Investment Advisers Act of 1940, as amended, providing non-discretionary and discretionary investment advice to its clients on an individual basis. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Fund Evaluation Group, LLC, Form ADV Part 2A & 2B can be obtained by written request directly to: Fund Evaluation Group, LLC, 201 East Fifth Street, Suite 1600, Cincinnati, OH 45202, Attention: Compliance Department.

The information herein was obtained from various sources. FEG does not guarantee the accuracy or completeness of such information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. FEG assumes no obligation to update this information, or to advise on further developments relating to it. FEG, its affiliates, directors, officers, employees, employee benefit programs and client accounts may have a long position in any securities of issuers discussed in this report.

Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell any securities.

Any return expectations provided are not intended as, and must not be regarded as, a representation, warranty or predication that the investment will achieve any particular rate of return over any particular time period or that investors will not incur losses.

Past performance is not indicative of future results.

The National Association of College and University Business Officers (NACUBO) is a membership organization representing more than 1900 colleges, universities and higher education service providers across the country. The NACUBO data was obtained from the 2023 NACUBO-TIAA Study of Endowments (NTSE), an independent third-party. The study includes a survey of 688 U.S. colleges and universities. The study divided the data into seven categories according to size of endowment, ranging from institutions with endowment assets under $25 million to those with assets in excess of $1 billion. The study data is for the 2023 fiscal year (July 1, 2022 - June 30, 2022) and based on the responses provided by the participants and is meant for illustration and educational purposes only. The average and median returns presented in this presentation are taken directly from the NACUBO study and were not calculated by or achieved by FEG or its clients. FEG is not affiliated with the organization and did not pay for the survey results.

This report is prepared for informational purposes only. It does not address specific investment objectives, or the financial situation and the particular needs of any person who may receive this report.

Fund Evaluation Group, LLC, Form ADV Part 2A & 2B can be obtained by written request directed to: Fund Evaluation Group, LLC, 201 East Fifth Street, Suite 1600, Cincinnati, OH 45202 Attention: Compliance Department.