-01.webp?width=400)

The outsourced chief investment officer (OCIO) investment model, with several notable advantages, continues to attract a growing number of institutional and nonprofit organizations. In this comprehensive guide, we provide key points from an insider’s perspective to help institutional investors evaluate OCIO providers.

Introduction

Since its inception in the late 1970s, the OCIO model has grown exponentially. In 2020, U.S. OCIO assets totaled $2.0 trillion and are expected to grow to $3.0 trillion by 2025.1 Along the way, the OCIO landscape has advanced from a fragmented, immature industry to a service mainstay. This maturity brings several important benefits to institutional investors interested in adopting the OCIO model, including more options in service providers and additional service options.

5 Steps to Hiring An OCIO

- Determine if an OCIO is Right for Your Organization

- Source Short List of OCIO Providers to Review

- Issue the RFP

- Make the Transition

- Maintain Oversight

STEP 1: Determine if an OCIO is Right for Your Organization

If your organization has not previously worked with an OCIO, you might have questions about whether the OCIO model is a better fiduciary fit for your organization. Committees and staff are often divided in their opinions of which model is ideal for the organization. However, it is important that all parties be aligned in the ultimate decision—whether it is to adopt an OCIO model or to maintain the organization’s current structure.

To make this decision, you will need to reflect candidly on your organization’s governance and have a solid understanding of the OCIO service model.

The Importance of Good Governance

The first step is assessing your organization’s governance process. In a typical governance structure, staff is responsible for the day-to-day oversight of the portfolio, while the investment/finance committee is responsible for the majority of the decision-making. The line between the two often gets blurred when different aspects of decision-making are delegated to staff, internal investment teams, consultants, and investment managers. While there are many different approaches to governance that can work, good governance must minimally allow for enough resources to oversee the investment portfolio as well as promote clear roles and responsibilities and effective decision-making.

Given that staff is often responsible for a myriad of other responsibilities outside of investment portfolio oversight, it is unsurprising that the main reason for outsourcing chief investment officer duties is small staff size. In a 2019 study from Cerulli Associates, 79% of respondents indicated they decided to outsource based on staffing limitations.2 The study also found the average investment team size for portfolios up to $5 billion was just one or two people. If your organization lacks sufficient resources for effective portfolio oversight, then it makes sense to consider how to increase your organization’s resources, possibly by adopting an OCIO model.

Next, consider whether the roles and responsibilities of the investment committee, investment consultant, and staff are clearly defined. Even when these roles are clearly defined in a well-crafted Investment Policy Statement (IPS), infrequent in-depth review of policy and rushed onboarding of new committee members can foster role ambiguity.

Good governance is vital regardless of service model. But beyond that, it is important to be honest about your oversight structure to determine which model is most appropriate.

Differences between OCIO and Consulting

The primary distinction between consulting and OCIO is discretion. In a consulting model, the investor or client retains discretion on both the strategy and implementation. In the OCIO model, the OCIO typically has full discretion over implementation, but may share discretion over the strategy.

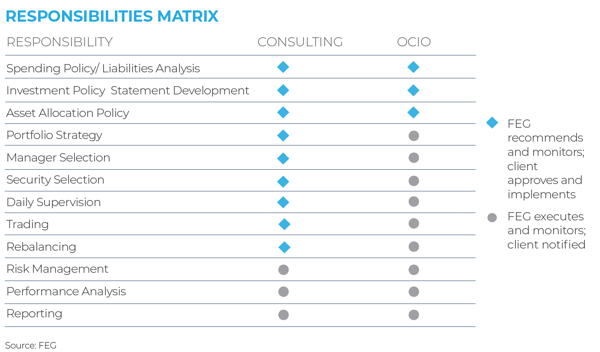

The OCIO and consulting models also have significant differences in the division of specific responsibilities. The Responsibilities Matrix below compares FEG’s OCIO with consulting models.

In both Consulting and OCIO, the investor typically determines high-level investment strategy and investment policy. The two service models diverge though in implementing that strategy. For the Consulting model, often committees make the decision of which funds to include and exclude in the portfolio with consultants informing the decision. For the OCIO model, the OCIO decides which funds go into and out of the portfolio, but within the guidelines of the IPS. Another potential difference between implementing strategy via the Consulting or OCIO model is that the latter generally provides a higher level of back-office support, although that is not always the case depending on individual service provider offerings.

FEG Insight

The OCIO model has rapidly gained in popularity and, in some client segments, such as higher education, surpasses the consulting model, with 52% of higher education institutions outsourcing.4 Other client segments have not embraced OCIO as rapidly, with only 24% of community foundations outsourcing.5 Although there are many reasons why institutions may elect not to outsource, one of the most commonly cited reasons is the desire to retain control.

For FEG, the client retains strategic control in both models. So perhaps the more impactful question is, “What is the highest and best use of committee and staff time?” It may very well be that one organization’s committee has the time and skills to directly oversee the implementation of the strategy by selecting managers, rebalancing, etc., while for other committees it might make sense to own just the strategy and outsource the implementation. The “right” answer to this question will vary, but asking the question and contrasting the answers against the responsibilities matrix will enable you to better assess the appropriate service model for your organization.

STEP 2: Source Short List of OCIO Providers to Review

There are a number of resources available to help you identify and source OCIO providers. One publicly available list is from Chief Investment Officer and is posted with their annual OCIO survey.

While the OCIO industry has evolved past the early stages of maturity, not all service providers are created equal. In general, there are two main categories of service providers: independent advisors and large asset managers. Both have something unique to offer, with general pros and cons highlighted below.

TYPES OF OCIO PROVIDERS |

|

|

Independent Providers |

Asset Managers / Banks |

|

PROS

|

PROS

|

|

CONS

|

CONS

|

A provider’s structure can be a helpful starting point for understanding its comparative strengths and weaknesses. To truly understand the profile of an individual firm, it is important to consider many aspects of the firm and ideally perform due diligence.

FEG Insight

While the strengths of the asset manager model are compelling, FEG believes independence matters. This helps ensure decisions are made on behalf of clients, and significantly reduces potential conflicts of interest.

STEP 3: Issuing the Request for Proposal

The request for proposal (RFP) process is complicated and involved, but can be manageable with good planning. FEG has responded to thousands of RFPs since our inception in 1988. We have seen an array of templates, processes, and timelines. We have synthesized the best practices into a comprehensive checklist and toolkit. This document includes a brief summary of those findings, but a more detailed explanation can be found here.

There are five key actions to the RFP process:

- Preparation

- Issuing the RFI

- Issuing the RFP

- Conducting Final Interviews

- Selection

ACTION |

RATIONALE |

|

Preparation |

Determining the Service Model: The RFP process usually goes smoother if the committee and staff are clear and united as to the preferred service model. If possible, try and seek consensus prior to submitting the RFP. Determining the Timeline: The process we recommend spans four months. While that may seem unpalatable, keep in mind that this is for relationships that often span five years or more, so careful consideration is due. To help begin your planning process, check out our sample service provider timeline template. Defining the Players: Often, a sub-committee of staff and either an investment or finance committee leads the selection process and reports back to the primary committee. Typically, the participating firms will need to be decided in this step. |

|

RFI |

Requests for information (RFIs) are typically shorter than RFPs and more focused on quantitative information. Issuing an RFI is often considered an optional step, as it will prolong the process. But RFIs may be helpful if you have identified more than 10 participating firms, are unsure which service model is appropriate, or have pre-defined criteria—e.g., minimum level of OCIO assets—that is important to share upfront. Ideally, an RFI phase will lead to a short list of 4-8 firms for the RFP. |

|

|

The RFP should provide more robust information than the RFI to help your organization gain an understanding of everything from investment approach to communication style. This is where you begin to assess compatibility. Additional questions should focus more heavily on resources, team, investment approach, risk management, and additional services. Once questions are defined, it is helpful to develop a scoring matrix to pre-determine the most important aspects to your organization and weight these areas accordingly. This will facilitate a smoother evaluation process. Ideally, an RFP phase will lead to a short list of 2-3 firms for the Finals. For a sample RFP scoring matrix, click here. |

|

|

Finals’ presentations are often structured as 45 minutes of formal presentation and 15 minutes of Q&A. If there are important questions to ask of the finalists, it is helpful to send these in advance to ensure the participant protects time to discuss. At this stage, unique questions are appropriate, and while it is fine to send a handful of topics all firms should cover, it is also acceptable to customize these for the individual participant. |

|

|

If, after the finals presentation, you are torn on which provider to hire, consider an on-site visit to view competitors’ respective offices and glean a better understanding of the firm’s culture, team, and resources. While it is an expense and costs time, this is meant to be a long-term partnership, so it is better to spend more time on the hiring process. Also, keep in mind that start dates should not occur mid-month if at all possible. This will help clarify and delineate the responsibilities of the exiting consultant and incoming advisor. The day after month-end is better, but immediately after the end of a quarter is ideal. |

FEG Insight

One tricky aspect of the RFP/finals process is deciding whether or not to request performance and how to evaluate it. Performance reporting is handled differently at various firms, which can make it difficult to assess. For example, there is a lot of discretion required when creating client composites – do you group by client type? Asset size? Asset allocation strategy? It is possible to have a number of clients with $50 million in assets who have significantly different risk/return profiles and corresponding asset allocation strategies. Including this breadth in the same composite can skew the results.

It can be difficult to circumvent all gray areas when making performance comparisons, but there are some considerations and questions that can get you a clear answer:

- Ask for the benchmarks used

- Ask if the organization is GIPS compliant, which sets rules for reporting performance that organizations must follow

- Clearly define the client types, sizes, allocation, and service models whose performance you would like to see

Fees are another aspect of selecting a service provider that can be confusing. There are many layers of fees, including the OCIO advisor fee, underlying manager fees, custodian fees, travel, operations, and other expenses. Like performance, fees can be misleading and confusing. For example, if a participant has their own product and plugs this product into the portfolio, they may be able to offer impressive OCIO advisor fees because the fees are being generated through the product.

We advise that you provide a table of all fees you would like to see broken out by the OCIO firms. You should also request to see the portfolio asset allocation, percent illiquid/semi-liquid/liquid, and percent active/passive to better understand why firms may differ in fee structures. For example, OCIO's proposing a highly active portfolio would intuitively have higher underlying manager fees than those proposing a more passive approach.

STEP 4: Make the Transition

The transition process to a new service provider is a highly underrated yet crucial step in the OCIO framework. Why is this important? Because if there is ambiguity around accountability, your interests—which should always be first priority—might not be as protected as they should be.

Once a strategy has been set, a new OCIO may want to adjust your organization’s portfolio as quickly as possible to align the portfolio with their views. This is generally a good thing, because it means the OCIO is likely conducting more in-depth due diligence on their strategies than the existing strategies, providing better oversight. But a transition that is too swift could expose the portfolio to unnecessary risks.

A swift transition could result in a large percentage of your portfolio being out-of-market at the same time. The timing of trades matter, and if you are unlucky on the direction of the markets, your OCIO may inadvertently sell low and buy high, resulting in loss of capital. This poor performance could be attributed to the exiting investment consultant or even the investment committee, but in truth, both the exiting consultant and incoming OCIO will have an influence on performance—the existing strategies may have gates and redemption windows that result in a transition spanning months or even years. Ultimately, the incoming OCIO is accountable for the transition.

- The first is to stage the transition so that only a certain percentage of the portfolio is out-of-market at any given point. FEG typically recommends that no more than 5-7% of the portfolio be out of the market during a transition process. Since March 2020, that figure has narrowed to 2-4% due to the higher risk associated with higher volatility.

- The other approach is to employ derivatives—e.g., futures contracts—to provide market exposure during the trade windows. This can be done directly by some of the larger firms, or can be outsourced to a transition manager for firms that do not provide the service internally.

Timing expectations.

Often, portfolios take months to fully transition (although for some with private investments it could take years). Paperwork needs to be submitted, operations need to process trades, and semi-liquid gates and redemption windows must be factored into the transition. The incoming OCIO should provide the committee and staff with regular status update on the transition process.

Termination of the prior consultant.

While it would be ideal if all consultants exited a terminating relationship gracefully, that is not always the case. Try and keep the time between the termination notice and termination date brief, bearing in mind that scheduling for the end of the quarter is preferred. Your new provider will need to work with your existing provider. If you can, help set expectations with the existing provider, then send an email or arrange a call introducing the existing consultant to the incoming provider. Good communications go a long way toward ensuring a seamless transition, and having your organization set expectations at the start increases the probability of a successful transition.Reporting continuity.

From a reporting standpoint, reporting should appear seamless from one service provider to the next and the new service provider should be expected to report past performance. Your exiting consultant should collaborate with the incoming OCIO and freely share information.

Contract language.

Add language into your contract with the new OCIO provider specifying how an eventual termination will be handled. Request that performance reports be provided over the covered periods—even post-termination. For example, if your institution terminates with the OCIO on December 31, the OCIO should still provide performance reports on the portfolio through December 31, even though these reports likely would not be produced until January at the earliest. Additionally, ask the incoming OCIO to clearly specify any additional fees that might occur.

STEP 5: Maintain Oversight

Oversight is a crucial component of a successful OCIO relationship. The OCIO is accountable for managing the portfolio and generating returns, but that should not equate to a black box. During the transition process, set clear expectations for the OCIO. When should they inform the committee of portfolio changes? How much detail is required on underlying strategies?

FEG recommends defining this language and incorporating it into the IPS. From there, you could create a matrix by which to conduct annual performance reviews. The OCIO should also self-assess at the same time, which can help reveal differences in perception and expectations between the OCIO and the committee.

In Conclusion

The OCIO landscape is ever-evolving and complex. You can use this document to gain clarity as to what your organization can expect as it seeks to explore OCIO as an option. We will continue to provide information related to industry trends and useful resources.

If you have any questions or suggestions, FEG would love to hear them!

3 FEG Flash Poll. FEG flash poll collected data from institutional investors in a wide variety of segments to provide insight on current topics. The poll included questions related to rebalancing following the March 2020 market lows. FEG received responses from 62 participants, the majority of which were from higher education organizations. More than 30% of the respondents indicated they manage over $1 billion in assets, and more than 66% indicated they use a consulting service model.

4 2019 NACUBO-TIAA Study of Endowments.

5 2022 FEG Community Foundation Survey. The study includes a survey of 98 U.S. Community Foundations. The survey was open for responses online from February 21 – April 8, 2022. Participants also had the option to complete their response as a Word document and email it back to FEG. The data from this survey was grouped into between five and seven categories based on assets of the community foundation, with assets ranging from less than $25 million to greater than $1 billion. The information in this study is based on the responses provided by the participants and is meant for illustration and educational purposes only.

DISCLOSURES

This report was prepared by Fund Evaluation Group, LLC (FEG), a federally registered investment adviser under the Investment Advisers Act of 1940, as amended, providing non-discretionary and discretionary investment advice to its clients on an individual basis. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser.

The information herein was obtained from various sources. FEG does not guarantee the accuracy or completeness of such information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. FEG assumes no obligation to update this information, or to advise on further developments relating to it.

Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell any securities.

Any return expectations provided are not intended as, and must not be regarded as, a representation, warranty or predication that the investment will achieve any particular rate of return over any particular time period or that investors will not incur losses.

Past performance is not indicative of future results.

This report is prepared for informational purposes only. It does not address specific investment objectives, or the financial situation and the particular needs of any person who may receive this report.

Fund Evaluation Group, LLC, Form ADV Part 2A & 2B can be obtained by written request directed to: Fund Evaluation Group, LLC, 201 East Fifth Street, Suite 1600, Cincinnati, OH 45202 Attention: Compliance Department.