"Interest rates are to asset prices what gravity is to the apple. When there are low rates, there is low gravitational pull on asset prices."

- Warren Buffet

Interest rates rose sharply during the quarter, reinstilling “gravity” into capital markets and pulling down asset prices across the board. This was particularly evident in the 73 basis point (bp) yield increase in the benchmark 10-Year U.S. Treasury Note, which had moved from 3.8% to 4.5% by quarter-end. Unlike physics, however, markets are not completely driven by formulaic laws. They are driven in part by participant’s reactions, which can be irrational in the short term. Or, as Isaac Newton said, “I can calculate the motion of heavenly bodies but not the madness of people.”

The “heavenly body” of the Federal Reserve System (Fed)—the Board of Governors—cannot be calculated either, but the board’s actions for the balance of the year will likely continue to have a major impact on where markets go next. To date, market participants have taken the Fed at its word as it relates to the commitment to restoring price stability and have positioned their portfolios accordingly. The Fed’s own projections, in the form of their closely followed “dot plot” and broader Summary of Economic Projections, suggests an additional 25 bps hike to the policy rate by the end of the year. Through quarter-end, the bond market, took a slightly less hawkish view given the fed funds futures offered roughly 40% odds the Fed will follow through with another hike by the conclusion of 2023.

When the dust settled on the quarter, most major asset classes had declined low-to-mid single digits, with longer-duration segments underperforming their shorter-duration brethren. Global equity markets, as measured by the MSCI All Country World Index, declined 3.4%. By industry sector, energy was a lone standout, generating a positive return on the quarter. Bonds and real assets, broadly speaking, were not additive, with the Bloomberg U.S. Aggregate Bond Index and S&P Real Assets Equity Index suffering losses of 3.2% and 4.6%, respectively. The HFXI Global Hedge Index, a rough proxy for hedge funds, generated a 0.8% return, outperforming most major stock, bond, and real asset indices, given its lower directional market exposure and typically short duration profile.

KEY MARKET THEMES AND DEVELOPMENTS

Surging Treasury Rates Send Ripples Throughout Financial Markets

Like the gravitational force on an apple falling from a tree, Treasury bond prices have plunged since the Fed embarked on its quest to normalize monetary policy in late 2021 amid the most robust inflationary impulse since the early 1980s. With a 525 bps increase to the federal funds rate since March 2022, market rates of interest—otherwise known as Treasury yields—have witnessed similar upward pressure, with the yield on the 10-Year U.S. Treasury Note surging to nearly 5% through the early trading days of October, the highest level since 2007.

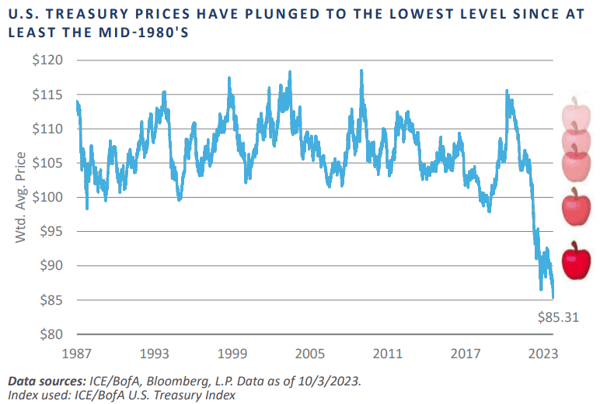

The outward shift in the Treasury yield curve in recent quarters has been so severe, the weighted-average price of outstanding Treasury securities has plummeted to its lowest level in the 30-plus years since the inception of the ICE/BofA U.S. Treasury Index, at a nearly 15-point discount versus par and more than 20 points below the historical average of $106.

Intuitively, the corners of the financial markets with the longest duration cash flow profiles, which are also those most sensitive to interest rate fluctuations, have faced the most significant performance headwinds, with growth-oriented equities—particularly smaller capitalization—long-duration fixed income sectors such as corporate credit, and real estate-related securities bearing most of the brunt.

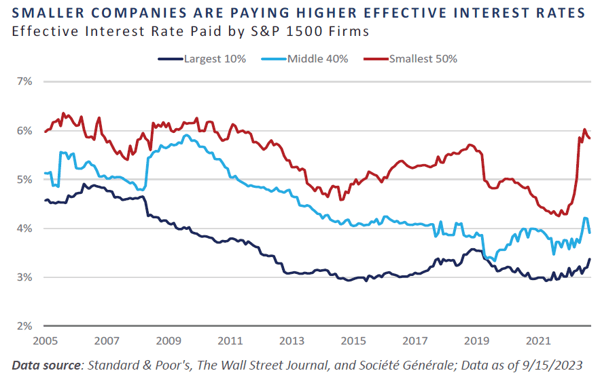

While smaller capitalization companies may appear relatively insulated from a deteriorating macro climate overseas versus their large cap brethren—especially companies that derive a disproportionate share of their revenue from Europe and China—smaller companies also operate with a higher cost of capital. According to research from Standard and Poor’s (S&P), the smallest 50% constituency of the S&P 1500 Composite Index pays an effective interest rate of approximately 6%, nearly double the rate paid by the largest 10% of the index.

Larger cap companies are not necessarily immune to the headwinds smaller companies face from the sharply rising cost of capital. During inflationary regimes in which policymakers are tasked with restoring price stability, particularly among economies grappling with a debt overhang, the correlation of stock and bond returns tends to rise. The rise in the cost of capital results in a lower net present value of future cashflows, in turn serving as a headwind to multiple expansion and earnings growth potential.

Through the third quarter, the rolling 3-year correlation in returns between U.S. large cap, as measured by the S&P 500, and core bonds, as measured by the Bloomberg U.S. Aggregate Bond Index, had ascended to 0.6, the highest level in the four decade-plus history of the core bond index. This connection served as a key performance headwind for traditional stock/bond portfolios in 2022 and in the trailing 2-month period.

One silver lining for investors possessing the willingness and ability to dynamically adjust risk postures based on prevailing market dynamics is the growing attractiveness of plain old Treasury securities at the expense of high-flying equities. Whereas the impact of Fed-induced monetary restraint seems to be rapidly transmitted into the bond market through quickly adjusting interest rate levels, equity valuations appear slower to respond.

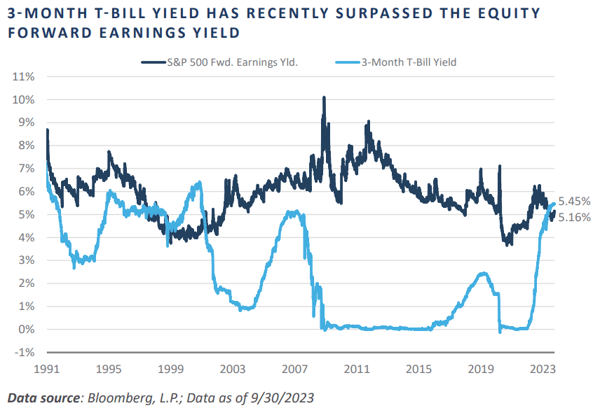

Some methods at teasing out the relative attractiveness of stocks versus bonds have evolved in recent months to buttress the case for a tactical overweight to bonds at the expense of equity risk. One example is the “Fed Model,” which compares the equity market earnings yield—i.e., inverse of the price-to-earnings multiple—versus the yield provided by a bond proxy, such as the front-end of the Treasury yield curve. Through the third quarter, the yield on the 3-Month T-Bill climbed almost 30 bps above the forward earnings yield on the S&P 500, implying the equity risk premium is at its narrowest versus the risk-free rate in more than two decades.

Private markets have also been forced to adjust to the rising cost of capital and warning risk tolerance in the market. The combination of less credit availability due to increasing interest rates, as well as declining valuations have led to a meaningful slowdown in deal activity and fundraising. This may lead to challenges for some 2020 and 2021 vintage year investments made prior to this reset that deployed capital quickly. Entry valuations are more attractive today for fresh capital being deployed going forward.

Private capital investing is a long-term endeavor and is difficult to time. Ultimately, finding good partners that can invest through different cycles, grow businesses and increase the value of assets is key. For growth-oriented investments this means a prudent purchase price and a growth plan ultimately to profitability. For buyout strategies this includes appropriate use of leverage and operational experience to drive value. For any investment, having multiple exit avenues will be important as the IPO window will open and close over time and higher rates may reduce the number of strategic acquirers and/or other private market managers with the ability to transact.

Policy Uncertainty

Ordinarily, long-run structural concerns such as the sustainability of fiscal and monetary policy are not included in a quarterly investment letter; however, certain developments in the post-Global Financial Crisis period, particularly following the global pandemic, are worth mentioning.

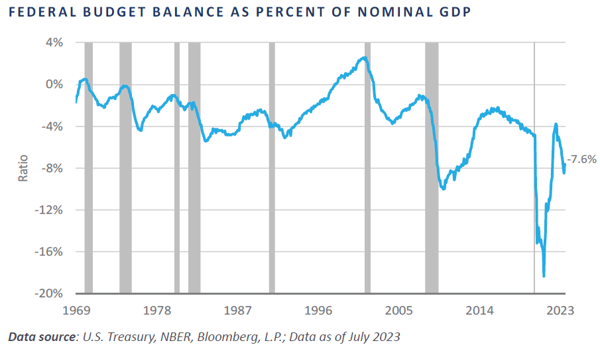

Repeated political stalemates resulting in debt limit standoffs and eleventh-hour resolutions, a downgrade of the U.S. sovereign credit by Fitch Ratings from AAA to AA+, the continued expansion of government social benefits, a deteriorating budget situation that stands to weaken further in the next downturn, a massive debt buildup across both the public and private sector, and incrementally more financial resources being directed toward interest expense—an unproductive use of capital—are all cause for concern.

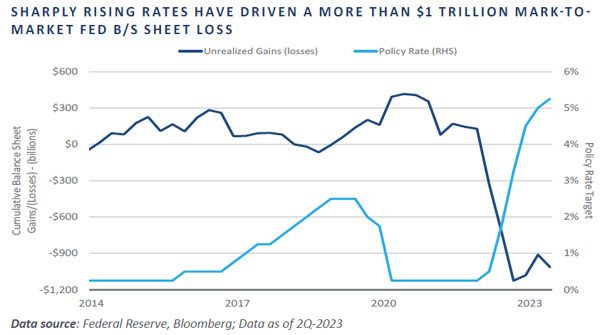

An additional, less commonly referenced issue has percolated in recent quarters. As the Fed has raised the policy rate in an effort to restore price stability, this has increased the interest rate on banking system reserves, which, despite the Fed’s tightening efforts since late 2021, still stand at more than $3 trillion. At 5.4%, this is one of the highest interest rates on the risk-free curve, exceeding all Treasury security yields beyond 1 year maturity as of 9/30/2023.

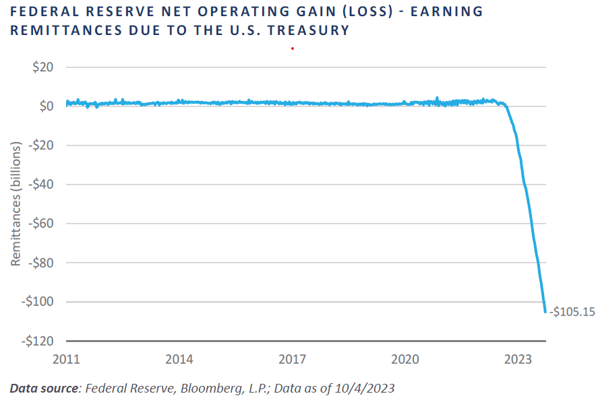

Significant Fed interest payments on commercial banking system reserves have led to a unique phenomenon in the Fed’s 110-year history—a net operating loss. This loss has swelled to more than $100 billion as of early October.

Typically, interest received by the Fed on its securities holdings more than offsets its operating expenses, leading to a net gain which is remitted to the Treasury, thereby helping to reduce the Treasury budget deficit. The more time that passes without the Fed lowering the policy rate—and thus the rate paid on reserve balances—the larger this loss may become. In turn, this could potentially drive the Treasury budget deficit even wider, which today stands just above levels witnessed during the 2007-2008 Global Financial Crisis.

The monetary problems do not end there, however. The Fed’s policy response to the global pandemic resulted in significant purchases of securities at very low yield levels—and thus high prices. The sharp rise across interest rates since 2020 has led to a meaningful drop in the market prices of the Fed’s security holdings. While the Fed is not required to mark its positions to market because it is expected to hold the securities until maturity, a significant portion of the Fed’s balance sheet assets are underwater.

As of the second quarter, the Fed’s Combined Quarterly Financial Report tables show the unrealized mark-to-market losses on the Fed’s security holdings amount to a staggering $1 trillion, versus a capital base of less than $60 billion.

The lagging nature of the impact of monetary policy on the economy and financial markets implies that even once the Fed formally pauses its tightening campaign, monetary restraint will continue to feed through the system without a policy pivot. Recent robustness displayed by the U.S. economy, including a further tightening in the labor market, in addition to headline and core inflation running materially above the Fed’s 2% target, suggest a pivot in Fed policy is far off in the distance.

A highly uncertain and generally concerning path of fiscal and monetary policy over the intermediate and longer-term horizon, combined with risk markets seemingly disconnected from a myriad of macroeconomic headwinds, continue to necessitate a particularly cautious investment approach with ongoing vigilance to identify compelling risk/return opportunities worth a flexing of risk budgets.

Reflections and Outlook

"Truth is ever to be found in the simplicity, and not the multiplicity and confusion of things." - Isaac Newton

Cash flow is the ultimate “truth” in investing. At present, the cash flow, or yield, on fixed income exceeds the earnings yield of equities. The cost of servicing debt in a higher rate environment further reduces cash flow and return potential for both public and private equity. As such, FEG continues to find fixed income relatively more attractive versus equities over the near term, given the better risk-adjusted return prospects.

However, markets tend to work over the long run, rewarding higher risk assets with higher commensurate returns. As such, FEG does not see a compelling reason to make major changes to long-term strategic asset allocations based solely upon the current market environment. Private market deal activity has slowed in 2023, but that will likely course correct over the long term. Therefore, FEG believes having as large a strategic allocation to private markets as is prudent for an investor’s unique situation will continue to ensure long-term returns.

FEG’s investment team is persistent in monitoring markets and investment managers for new investments and ideas to present themselves, but there is a dearth of compelling new investment opportunities at this point in the cycle. Ultimately, the natural ebbs and flows of markets will offer up new investments and the team aims to be ready to act when these positions are identified. As Warren Buffett said, “We don’t have to be smarter than the rest. We have to be more disciplined than the rest.”

DISCLOSURES

This report was prepared by FEG (also known as Fund Evaluation Group, LLC), a federally registered investment adviser under the Investment Advisers Act of 1940, as amended, providing non-discretionary and discretionary investment advice to its clients on an individual basis. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Fund Evaluation Group, LLC, Form ADV Part 2A & 2B can be obtained by written request directly to: Fund Evaluation Group, LLC, 201 East Fifth Street, Suite 1600, Cincinnati, OH 45202, Attention: Compliance Department.

The information herein was obtained from various sources. FEG does not guarantee the accuracy or completeness of such information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. FEG assumes no obligation to update this information, or to advise on further developments relating to it. FEG, its affiliates, directors, officers, employees, employee benefit programs and client accounts may have a long position in any securities of issuers discussed in this report.

Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material or guarantee the accuracy or completeness of any information herein, nor does Bloomberg make any warranty, express or implied, as to the results to be obtained therefrom, and, to the maximum extent allowed by law, Bloomberg shall not have any liability or responsibility for injury or damages arising in connection therewith

Index performance results do not represent any managed portfolio returns. An investor cannot invest directly in a presented index, as an investment vehicle replicating an index would be required. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown.

The Chartered Financial Analyst® (CFA) designation is a professional certification issued by the CFA Institute to qualified financial analysts who: (i) have a bachelor’s degree and four years of professional experience involving investment decision making or four years of qualified work experience[full time, but not necessarily investment related]; (ii) complete a self‐study program (250 hours of study for each of the three levels); (iii) successfully complete a series of three six‐hour exams; and (iv) pledge to adhere to the CFA Institute Code of Ethics and Standards of Professional Conduct.

The Chartered Alternative Investment Analyst Association® is an independent, not‐for‐profit global organization committed to education and professionalism in the field of alternative investments. Founded in 2002, the CAIA Association is the sponsoring body for the CAIA designation. Recognized globally, the designation certifies one's mastery of the concepts, tools and practices essential for understanding alternative investments and promotes adherence to high standards of professional conduct.

Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell any securities.

Any return expectations provided are not intended as, and must not be regarded as, a representation, warranty or predication that the investment will achieve any particular rate of return over any particular time period or that investors will not incur losses.

Diversification or Asset Allocation does not assure or guarantee better performance and cannot eliminate the risk of investment loss.

Past performance is not indicative of future results.

This blog is prepared for informational purposes only. It does not address specific investment objectives, or the financial situation and the particular needs of any person who may receive this report.

INDICES

The Alerian MLP Index is a composite of the 50 most prominent energy Master Limited Partnerships that provides investors with an unbiased, comprehensive benchmark for this emerging asset class.

The HFRI Monthly Indices (HFRI) are equally weighted performance indexes, compiled by Hedge Fund Research Inc., and are utilized by numerous hedge fund managers as a benchmark for their own hedge funds. The HFRI are broken down into 37 different categories by strategy, including the HFRI Fund Weighted Composite, which accounts for over 2000 funds listed on the internal HFR Database. The HFRI Fund of Funds Composite Index is an equal weighted, net of fee, index composed of approximately 800 fund of funds which report to HFR. See www.hedgefundresearch.com for more information on index construction.

The MSCI ACWI (All Country World Index) Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI consists of 47 country indexes comprising 23 developed and 24 emerging market country indexes. The developed market country indexes included are: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The emerging market country indexes included are: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar,Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and United Arab Emirates.

The S&P 500 Index is a capitalization-weighted index of 500 stocks. The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Information on any indices mentioned can be obtained either through your advisor or by written request to information@feg.com.

Market Insight

Third Quarter 2023 Market Commentary: Gravity's Impact on Markets

"Interest rates are to asset prices what gravity is to the apple. When there are low rates, there is low gravitational pull on asset prices."

- Warren Buffet

Interest rates rose sharply during the quarter, reinstilling “gravity” into capital markets and pulling down asset prices across the board. This was particularly evident in the 73 basis point (bp) yield increase in the benchmark 10-Year U.S. Treasury Note, which had moved from 3.8% to 4.5% by quarter-end. Unlike physics, however, markets are not completely driven by formulaic laws. They are driven in part by participant’s reactions, which can be irrational in the short term. Or, as Isaac Newton said, “I can calculate the motion of heavenly bodies but not the madness of people.”

The “heavenly body” of the Federal Reserve System (Fed)—the Board of Governors—cannot be calculated either, but the board’s actions for the balance of the year will likely continue to have a major impact on where markets go next. To date, market participants have taken the Fed at its word as it relates to the commitment to restoring price stability and have positioned their portfolios accordingly. The Fed’s own projections, in the form of their closely followed “dot plot” and broader Summary of Economic Projections, suggests an additional 25 bps hike to the policy rate by the end of the year. Through quarter-end, the bond market, took a slightly less hawkish view given the fed funds futures offered roughly 40% odds the Fed will follow through with another hike by the conclusion of 2023.

When the dust settled on the quarter, most major asset classes had declined low-to-mid single digits, with longer-duration segments underperforming their shorter-duration brethren. Global equity markets, as measured by the MSCI All Country World Index, declined 3.4%. By industry sector, energy was a lone standout, generating a positive return on the quarter. Bonds and real assets, broadly speaking, were not additive, with the Bloomberg U.S. Aggregate Bond Index and S&P Real Assets Equity Index suffering losses of 3.2% and 4.6%, respectively. The HFXI Global Hedge Index, a rough proxy for hedge funds, generated a 0.8% return, outperforming most major stock, bond, and real asset indices, given its lower directional market exposure and typically short duration profile.

KEY MARKET THEMES AND DEVELOPMENTS

Surging Treasury Rates Send Ripples Throughout Financial Markets

Like the gravitational force on an apple falling from a tree, Treasury bond prices have plunged since the Fed embarked on its quest to normalize monetary policy in late 2021 amid the most robust inflationary impulse since the early 1980s. With a 525 bps increase to the federal funds rate since March 2022, market rates of interest—otherwise known as Treasury yields—have witnessed similar upward pressure, with the yield on the 10-Year U.S. Treasury Note surging to nearly 5% through the early trading days of October, the highest level since 2007.

The outward shift in the Treasury yield curve in recent quarters has been so severe, the weighted-average price of outstanding Treasury securities has plummeted to its lowest level in the 30-plus years since the inception of the ICE/BofA U.S. Treasury Index, at a nearly 15-point discount versus par and more than 20 points below the historical average of $106.

Intuitively, the corners of the financial markets with the longest duration cash flow profiles, which are also those most sensitive to interest rate fluctuations, have faced the most significant performance headwinds, with growth-oriented equities—particularly smaller capitalization—long-duration fixed income sectors such as corporate credit, and real estate-related securities bearing most of the brunt.

While smaller capitalization companies may appear relatively insulated from a deteriorating macro climate overseas versus their large cap brethren—especially companies that derive a disproportionate share of their revenue from Europe and China—smaller companies also operate with a higher cost of capital. According to research from Standard and Poor’s (S&P), the smallest 50% constituency of the S&P 1500 Composite Index pays an effective interest rate of approximately 6%, nearly double the rate paid by the largest 10% of the index.

Larger cap companies are not necessarily immune to the headwinds smaller companies face from the sharply rising cost of capital. During inflationary regimes in which policymakers are tasked with restoring price stability, particularly among economies grappling with a debt overhang, the correlation of stock and bond returns tends to rise. The rise in the cost of capital results in a lower net present value of future cashflows, in turn serving as a headwind to multiple expansion and earnings growth potential.

Through the third quarter, the rolling 3-year correlation in returns between U.S. large cap, as measured by the S&P 500, and core bonds, as measured by the Bloomberg U.S. Aggregate Bond Index, had ascended to 0.6, the highest level in the four decade-plus history of the core bond index. This connection served as a key performance headwind for traditional stock/bond portfolios in 2022 and in the trailing 2-month period.

One silver lining for investors possessing the willingness and ability to dynamically adjust risk postures based on prevailing market dynamics is the growing attractiveness of plain old Treasury securities at the expense of high-flying equities. Whereas the impact of Fed-induced monetary restraint seems to be rapidly transmitted into the bond market through quickly adjusting interest rate levels, equity valuations appear slower to respond.

Some methods at teasing out the relative attractiveness of stocks versus bonds have evolved in recent months to buttress the case for a tactical overweight to bonds at the expense of equity risk. One example is the “Fed Model,” which compares the equity market earnings yield—i.e., inverse of the price-to-earnings multiple—versus the yield provided by a bond proxy, such as the front-end of the Treasury yield curve. Through the third quarter, the yield on the 3-Month T-Bill climbed almost 30 bps above the forward earnings yield on the S&P 500, implying the equity risk premium is at its narrowest versus the risk-free rate in more than two decades.

Private markets have also been forced to adjust to the rising cost of capital and warning risk tolerance in the market. The combination of less credit availability due to increasing interest rates, as well as declining valuations have led to a meaningful slowdown in deal activity and fundraising. This may lead to challenges for some 2020 and 2021 vintage year investments made prior to this reset that deployed capital quickly. Entry valuations are more attractive today for fresh capital being deployed going forward.

Private capital investing is a long-term endeavor and is difficult to time. Ultimately, finding good partners that can invest through different cycles, grow businesses and increase the value of assets is key. For growth-oriented investments this means a prudent purchase price and a growth plan ultimately to profitability. For buyout strategies this includes appropriate use of leverage and operational experience to drive value. For any investment, having multiple exit avenues will be important as the IPO window will open and close over time and higher rates may reduce the number of strategic acquirers and/or other private market managers with the ability to transact.

Policy Uncertainty

Ordinarily, long-run structural concerns such as the sustainability of fiscal and monetary policy are not included in a quarterly investment letter; however, certain developments in the post-Global Financial Crisis period, particularly following the global pandemic, are worth mentioning.

Repeated political stalemates resulting in debt limit standoffs and eleventh-hour resolutions, a downgrade of the U.S. sovereign credit by Fitch Ratings from AAA to AA+, the continued expansion of government social benefits, a deteriorating budget situation that stands to weaken further in the next downturn, a massive debt buildup across both the public and private sector, and incrementally more financial resources being directed toward interest expense—an unproductive use of capital—are all cause for concern.

An additional, less commonly referenced issue has percolated in recent quarters. As the Fed has raised the policy rate in an effort to restore price stability, this has increased the interest rate on banking system reserves, which, despite the Fed’s tightening efforts since late 2021, still stand at more than $3 trillion. At 5.4%, this is one of the highest interest rates on the risk-free curve, exceeding all Treasury security yields beyond 1 year maturity as of 9/30/2023.

Significant Fed interest payments on commercial banking system reserves have led to a unique phenomenon in the Fed’s 110-year history—a net operating loss. This loss has swelled to more than $100 billion as of early October.

Typically, interest received by the Fed on its securities holdings more than offsets its operating expenses, leading to a net gain which is remitted to the Treasury, thereby helping to reduce the Treasury budget deficit. The more time that passes without the Fed lowering the policy rate—and thus the rate paid on reserve balances—the larger this loss may become. In turn, this could potentially drive the Treasury budget deficit even wider, which today stands just above levels witnessed during the 2007-2008 Global Financial Crisis.

The monetary problems do not end there, however. The Fed’s policy response to the global pandemic resulted in significant purchases of securities at very low yield levels—and thus high prices. The sharp rise across interest rates since 2020 has led to a meaningful drop in the market prices of the Fed’s security holdings. While the Fed is not required to mark its positions to market because it is expected to hold the securities until maturity, a significant portion of the Fed’s balance sheet assets are underwater.

As of the second quarter, the Fed’s Combined Quarterly Financial Report tables show the unrealized mark-to-market losses on the Fed’s security holdings amount to a staggering $1 trillion, versus a capital base of less than $60 billion.

The lagging nature of the impact of monetary policy on the economy and financial markets implies that even once the Fed formally pauses its tightening campaign, monetary restraint will continue to feed through the system without a policy pivot. Recent robustness displayed by the U.S. economy, including a further tightening in the labor market, in addition to headline and core inflation running materially above the Fed’s 2% target, suggest a pivot in Fed policy is far off in the distance.

A highly uncertain and generally concerning path of fiscal and monetary policy over the intermediate and longer-term horizon, combined with risk markets seemingly disconnected from a myriad of macroeconomic headwinds, continue to necessitate a particularly cautious investment approach with ongoing vigilance to identify compelling risk/return opportunities worth a flexing of risk budgets.

Reflections and Outlook

"Truth is ever to be found in the simplicity, and not the multiplicity and confusion of things." - Isaac Newton

Cash flow is the ultimate “truth” in investing. At present, the cash flow, or yield, on fixed income exceeds the earnings yield of equities. The cost of servicing debt in a higher rate environment further reduces cash flow and return potential for both public and private equity. As such, FEG continues to find fixed income relatively more attractive versus equities over the near term, given the better risk-adjusted return prospects.

However, markets tend to work over the long run, rewarding higher risk assets with higher commensurate returns. As such, FEG does not see a compelling reason to make major changes to long-term strategic asset allocations based solely upon the current market environment. Private market deal activity has slowed in 2023, but that will likely course correct over the long term. Therefore, FEG believes having as large a strategic allocation to private markets as is prudent for an investor’s unique situation will continue to ensure long-term returns.

FEG’s investment team is persistent in monitoring markets and investment managers for new investments and ideas to present themselves, but there is a dearth of compelling new investment opportunities at this point in the cycle. Ultimately, the natural ebbs and flows of markets will offer up new investments and the team aims to be ready to act when these positions are identified. As Warren Buffett said, “We don’t have to be smarter than the rest. We have to be more disciplined than the rest.”

DISCLOSURES

This report was prepared by FEG (also known as Fund Evaluation Group, LLC), a federally registered investment adviser under the Investment Advisers Act of 1940, as amended, providing non-discretionary and discretionary investment advice to its clients on an individual basis. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Fund Evaluation Group, LLC, Form ADV Part 2A & 2B can be obtained by written request directly to: Fund Evaluation Group, LLC, 201 East Fifth Street, Suite 1600, Cincinnati, OH 45202, Attention: Compliance Department.

The information herein was obtained from various sources. FEG does not guarantee the accuracy or completeness of such information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. FEG assumes no obligation to update this information, or to advise on further developments relating to it. FEG, its affiliates, directors, officers, employees, employee benefit programs and client accounts may have a long position in any securities of issuers discussed in this report.

Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material or guarantee the accuracy or completeness of any information herein, nor does Bloomberg make any warranty, express or implied, as to the results to be obtained therefrom, and, to the maximum extent allowed by law, Bloomberg shall not have any liability or responsibility for injury or damages arising in connection therewith

Index performance results do not represent any managed portfolio returns. An investor cannot invest directly in a presented index, as an investment vehicle replicating an index would be required. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown.

The Chartered Financial Analyst® (CFA) designation is a professional certification issued by the CFA Institute to qualified financial analysts who: (i) have a bachelor’s degree and four years of professional experience involving investment decision making or four years of qualified work experience[full time, but not necessarily investment related]; (ii) complete a self‐study program (250 hours of study for each of the three levels); (iii) successfully complete a series of three six‐hour exams; and (iv) pledge to adhere to the CFA Institute Code of Ethics and Standards of Professional Conduct.

The Chartered Alternative Investment Analyst Association® is an independent, not‐for‐profit global organization committed to education and professionalism in the field of alternative investments. Founded in 2002, the CAIA Association is the sponsoring body for the CAIA designation. Recognized globally, the designation certifies one's mastery of the concepts, tools and practices essential for understanding alternative investments and promotes adherence to high standards of professional conduct.

Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell any securities.

Any return expectations provided are not intended as, and must not be regarded as, a representation, warranty or predication that the investment will achieve any particular rate of return over any particular time period or that investors will not incur losses.

Diversification or Asset Allocation does not assure or guarantee better performance and cannot eliminate the risk of investment loss.

Past performance is not indicative of future results.

This blog is prepared for informational purposes only. It does not address specific investment objectives, or the financial situation and the particular needs of any person who may receive this report.

INDICES

The Alerian MLP Index is a composite of the 50 most prominent energy Master Limited Partnerships that provides investors with an unbiased, comprehensive benchmark for this emerging asset class.

The HFRI Monthly Indices (HFRI) are equally weighted performance indexes, compiled by Hedge Fund Research Inc., and are utilized by numerous hedge fund managers as a benchmark for their own hedge funds. The HFRI are broken down into 37 different categories by strategy, including the HFRI Fund Weighted Composite, which accounts for over 2000 funds listed on the internal HFR Database. The HFRI Fund of Funds Composite Index is an equal weighted, net of fee, index composed of approximately 800 fund of funds which report to HFR. See www.hedgefundresearch.com for more information on index construction.

The MSCI ACWI (All Country World Index) Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI consists of 47 country indexes comprising 23 developed and 24 emerging market country indexes. The developed market country indexes included are: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The emerging market country indexes included are: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar,Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and United Arab Emirates.

The S&P 500 Index is a capitalization-weighted index of 500 stocks. The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Information on any indices mentioned can be obtained either through your advisor or by written request to information@feg.com.

Recent posts

Subscribe to blog