-01.webp?width=400)

Yes, but…

the many nuances of the endowment model

Over the past 30+ years FEG has been in business, we have been fortunate to work on behalf of some amazing endowments and foundations. As such, we have developed a unique view of what the “endowment model” means, how it should be executed, and how it will evolve. The endowment model has been mentioned several times in the press of late due to the unfortunate passing of key architect and longtime chief investment officer of Yale University’s investment office, David Swensen. Additionally, Larry Siegel and Richard Ennis have been engaged in a public debate over the pros and cons of this unique style of investing. 1

One overarching advantage endowments have over other pools of capital is a long time horizon. Endowments defy the two certainties in life: death and taxes. This provides the luxury to think and invest for the long term, which can be expressed in different ways via portfolio construction. Moreover, fully capturing the benefit of a long-term approach requires the buy-in of the organization as well as all parties involved in the organization’s decision-making.

Given the debate over the efficacy of the endowment model, we felt compelled to articulate what it means to us and where we see “the puck going,” as it were, in hockey terms. It is also worth noting that these comments are geared generally towards organizations with an appropriate governance model and sufficient infrastructure to handle the associated investment and operational complexity. We outline the key tenets of classic endowment model principles and share our view on each in turn.

1 https://larrysiegel.org/is-the-endowment-model-a-good-investment-strategy/

Endowment Model Principles

Equity Bias

Equity Bias

Ownership vs. creditorship to drive return. Embrace the risk and reward of capitalism and the ability of entrepreneurs to create value.

Illiquidity Premium

Illiquidity Premium

Be a provider of liquidity to garner excess returns, as investors tend to overvalue liquidity.

Diversification

Diversification

Spreading risk assets broadly allows for a lower allocation to bonds and cash to increase return without a meaningful increase in total portfolio risk.

Manager Alpha

Manager Alpha

Seek out active managers who can exploit market inefficiencies in particular areas of the market with greater alpha potential. Typically defined as the spread between top and bottom quartile managers.

FEG View

Equity Bias

Yes, have an equity bias, but... maintaining an equity bias is nuanced and needs to factor in the magnitude of the bias as well as the implementation strategy. We should highlight that our definition of equities for an endowment includes both public and private equity, and we want to have a bias to both. Other important considerations include geographical diversification, active vs. passive, and style choice, such as growth or value. Additionally, the current market background and the “there-is-no-alternative” (TINA) mentality regarding equities can be somewhat disquieting when thinking about setting asset allocation looking forward.

Within public equity, most endowment model advocates favor active management over passive/index management. FEG has also seen a bias for fundamental managers versus quantitative styles of management, and within fundamental stock pickers, a bias toward those that tend to run more concentrated portfolios versus highly diversified. We generally agree with this approach, but we also employ indexing and will consider quantitative approaches selectively. FEG also maintains that it is challenging to outperform the public equity market net of fees–especially in large, liquid, developed markets—and therefore advocate for the discerning selection of managers.

Global diversification of public equities has led to lower returns over the past decade, with the U.S. stock market outperforming most non-U.S. markets. Not all decades are the same however, and maintaining global diversification of public equity allocations remains a reasonable approach. Global market capitalization is a good starting point for developing an allocation in lieu of a strong view as to which areas of public equity markets will perform better or worse. In today’s market, that would result in roughly a 60% allocation to U.S. equities and 40% to non-U.S. equities.

In the private market, FEG takes the view that private equity provides largely the same equity risk as the public equity market, but with more upside if done right. Private equity has been and will continue to be an important part of endowment portfolios. Historical returns have been good, but these returns have attracted a remarkable influx of new capital. Ultimately, to continue delivering the returns that endowments need from private equity, investors need to get a few things right, the first of which is careful manager selection.

A thoughtful private equity implementation strategy is also important. For example, FEG believes successful mega-buyouts and generalist funds will have a harder time generating a premium over public markets, given the flood of capital. Lower middle market managers with sector specialization have demonstrated greater dispersion of returns across the population of managers. Therefore, if one can identify top quartile managers, one should find more reward and better return potential, in our opinion. This makes intuitive sense, as buying smaller businesses is somewhat less competitive and less expensive. Small businesses also offer more room to add value through operational improvements by private equity managers with deep sector expertise.

One additional tool that can be used to combat lower return potential and the higher fees of private equity is to build a co-investment program with fund managers. Some private equity managers will offer no-fee, no-carry co-investment opportunities in the businesses they buy when the equity check needed is larger than the manager can write out of their fund. Getting into the flow of co-investments takes a concerted effort which requires the ability to react quickly—given that most timelines are short—and the legal and operational infrastructure necessary to support a program of this kind; however, once built, the eradication of a 2% management fee and 20% carry can go a long way toward increasing net-of-fee returns.

From a portfolio construction standpoint, having a balance of private equity funds is also wise. Buyout funds are typically more value-oriented, while growth equity and venture capital are growth-focused. FEG believes that resisting the urge to tilt too far in either direction is prudent, however, the past year has seen phenomenal performance from venture capital, which has led many endowments to become heavily tilted toward growth in general and the technology sector in particular. Within venture capital, we believe biotech is poised for continued innovation and return potential in the decades to come and is therefore an area to which endowments should be looking to increase exposure.

Lastly, public and private market investors have collided, and the invention now has a name: “crossover investors.” This began in the early 2000s when tech public market investors such as Tiger Global and Coatue started investing in private companies. The crossover approach has since become much more prevalent, particularly in tech and biotech. Innovation within public companies will impact private companies and vice versa. If a manager invests solely in public or only private businesses, they are only hearing half the story. These crossover funds are another new pool in which a well-balanced endowment portfolio may have some allocation.

Illiquidity Premium

Yes, embrace illiquidity, but... where there is compensation for being a provider of liquidity will evolve over time. FEG is not convinced there currently is an illiquidity premium sufficient to overcome fees in mainstream hedge fund and leveraged buyout (LBO) strategies. This is because increased acceptance of these strategies has spawned growth in the number of managers and capital invested in these areas, which has led to increased competition and ultimately lowered returns for the average manager. Version 1.0 of “alternatives” is now a pure manager selection game, as dispersion between managers remains, but the asset classes at large no longer have the lower prices and less competition wind at their back that created the illiquidity premium in the first place. Therefore, capturing an illiquidity premium today requires investors to look further afield in “alternatives to alternatives.” Time will tell which areas offer up the best return potential, although they could include areas like royalties, litigation finance, carbon tax credits, etc.

At the total portfolio level, we believe one should maximize the ability to invest in less liquid assets while still being mindful of having sufficient liquidity. This includes several items. First is ensuring there is readily available capital to meet any near-term cash needs. Second is managing and monitoring the liquidity schedules of managers that offer less than daily, but periodic liquidity windows to withdrawal capital such as hedge funds. Last, but certainly not least, is the development and ongoing management of a commitment pacing schedule for truly illiquid assets. These tend to be invested via fund structures, where an investor commits capital to a manager who will call that capital down over a three-to-five-year period. Thus, one needs to ensure the current market value, as well as the amount of uncalled capital, is monitored and managed in a prudent fashion.

DIVERSIFICATION

Yes, diversify, but... one can take any good idea too far. The trade-off between diversification and return potential is a continual balancing act. Some asset classes and strategies may be diversifying but may not have the return potential sufficient to make them additive to the total portfolio. Also, as capital flows into alternative asset classes that were once diversifying, those flows can change the dynamics of those classes over time. The increased asset flows, liquidity, and price discovery that occur as an asset class matures tend to increase correlation to primary market risks, namely equity markets and interest rates. Therefore, if an investment is being made in the name of diversification, verify that the diversification benefits are actually present.

Any conversation on diversification and the endowment model must also touch on hedge funds. Looking forward, we expect the size and composition of allocations to evolve. As the industry has matured—now with more than $4 trillion in assets under management (AUM)—returns continue to decline.

Ironically, the need for what hedge funds promise, namely return streams uncorrelated with the stock market, seems to be greater than ever, given that historically low interest rates have created an unholy triumvirate of:

1) low returns on bonds,

2) higher valuations on equities, and

3) increased risk of correlation of stocks and bonds, if and when, rates do go up.

With bonds poised to deliver approximately 2%, the potential of earning 5-7% from a hedge fund portfolio with reasonably modest levels of volatility and correlation to equities makes this a compelling option. That said, FEG anticipates that hedge fund allocations will come down and evolve. Large endowments have historically held hedge fund allocations of around 20%, but FEG believes that number is likely to decrease to 15%, or lower, in the future. We also believe that other private diversifying assets, such as the “alternative to alternatives” mentioned in the illiquidity premium section, will be used more often to complement hedge funds for diversification with better return potential.

The final point on diversification would be the historically large allocation, 10-20%, to real assets for endowments. Given part of the rationale for owning real assets has been inflation protection, and we have experienced little to no inflation over the past three decades, endowments are a bit leery on real assets.

Additionally, historical allocations included meaningful investment in energy assets, which have been prolific at destroying capital investing and are also out of favor given the rise of ESG and divestment of fossil fuel movements. That said, FEG does think real assets will play a role in the future, but they will need to evolve to include both the old economy and the new economy; things like IT infrastructure to support the build-out of 5G, data centers, and renewable energy ought to be considered in addition to traditional energy and real estate assets.

MANAGER ALPHA

Yes, seek alpha, but... do so with eyes wide open. Always keep in mind that alpha can be positive or negative, driving the need for a well-defined top-down strategy for investing in active managers, as well as a dedicated investment team to execute said strategy. Also, from a bottom-up standpoint, allocators can think through competitive advantages they have versus other allocators in sourcing and accessing best-in-class managers.

In terms of top-down strategy, large, liquid markets tend to have less alpha potential, which means fees matter more and should be lower. In smaller, less liquid markets, there tend to be more pricing inefficiencies and therefore greater alpha potential. Additionally, many smaller, less liquid markets lack the availability of index funds, which makes active management the only option for gaining exposure. Importantly, asset classes will change over time on this continuum of more/less efficiency, and investment strategy must evolve to keep pace.

As markets become more competitive, active management has become increasingly specialized to provide managers an “edge” in their respective corners of the market. This has brought about the rise of manager specialists. Within both public and private equities, specialists have many different areas where they can focus, including company size, developed vs. emerging markets, or sector specialists with unique domain expertise. Conducting manager due diligence on specialists requires the humility to recognize you cannot be an expert at everything as well as the discipline to focus due diligence efforts on a small number of opportunities with high alpha potential.

Once the top-down strategy and areas of focus on specialist managers are set, then the hard work of sourcing and diligence of managers begins. One tenet FEG looks for in active managers is alignment of interest. This can take many forms, including how a manager is paid, having fees linked to excess return generated, and a manager’s personal investment in the fund. Additionally, newer and emerging managers offer another source of potential alignment. Generally, such firms are created when an investor leaves a more established firm and essentially bets their career on starting a new firm, making such individuals typically highly motivated to do whatever it takes to ensure their new enterprise is successful.

Manager research is about more than just alignment, however. Like most things in life, one tends to get better with practice. Having experienced teams focused on manager sourcing and due diligence is imperative. Experienced teams also tend to build relationships in the industry, which creates a broad sourcing funnel to generate a large universe of managers to vet. Lastly, many of the best-in-class active managers tend to be capacity constrained, with investor demand that often exceeds the limited size of their funds. Therefore, building relationships with these managers and working hard to gain access to them is critical.

GOVERNANCE

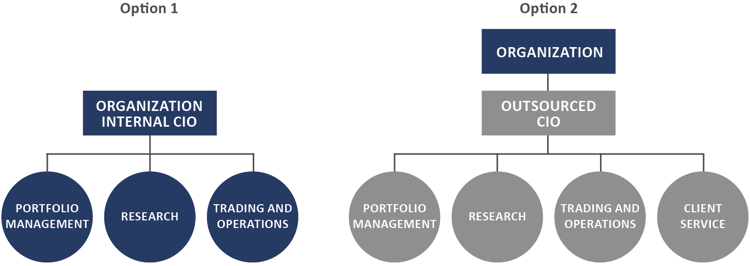

Once these principles are in place, the final prerequisite for an endowment style of investing to be successful is the appropriate governance structure and the right investment team in place to execute the investment strategy. Although there are a few exceptions, this typically takes one of two forms. First is an organization with a large enough pool of assets to build a dedicated internal investment office to implement the investment strategy with the support and blessing of their investment committee. The second is an organization with a smaller asset size or some other structural limitation which makes it impossible to build and support an internal investment office; in this case, an outsourced CIO (OCIO) partner can implement an endowment model solution on the organization’s behalf.

CONCLUDING THOUGHTS

In managing long-term pools of capital, FEG believes organizations benefit from ensuring the right governance structure is in place to support the investment strategy. If an endowment model strategy is adopted, in addition to appropriate governance, there are four key principles that need to be addressed. Having a view of each of these principles and developing a game plan for how the investment strategy will be executed within each principle is likely to benefit the endowment for years to come. Finally, having an open mind and being willing to evolve or change how to implement the investment strategy within each of the four principles will further help increase the odds of success.

DISCLOSURES

This report was prepared by FEG (also known as Fund Evaluation Group, LLC), a federally registered investment adviser under the Investment Advisers Act of 1940, as amended, providing non-discretionary and discretionary investment advice to its clients on an individual basis. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Fund Evaluation Group, LLC, Form ADV Part 2A & 2B can be obtained by written request directly to: Fund Evaluation Group, LLC, 201 East Fifth Street, Suite 1600, Cincinnati, OH 45202, Attention: Compliance Department.

The information herein was obtained from various sources. FEG does not guarantee the accuracy or completeness of such information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. FEG assumes no obligation to update this information, or to advise on further developments relating to it. FEG, its affiliates, directors, officers, employees, employee benefit programs and client accounts may have a long position in any securities of issuers discussed in this report.

Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell any securities.

Past performance is not indicative of future results.

This report is prepared for informational purposes only. It does not address specific investment objectives, or the financial situation and the particular needs of any person who may receive this report..

Published October 2021