FEG returned to China this spring for the first time since the COVID-19 pandemic began. While there, we visited Shenzhen and Hong Kong, attended a China-focused investment conference, and met with 13 managers across public equity, private equity, and hedge funds. In addition, we consumed large amounts of research and data in preparation for this trip. The following is a synthesis of our learnings and observations. It is only a point in time during a dynamic economic and geopolitical time. It is organized by the main piece, China: The Good, the Bad, and the Pragmatic, and followed by short essays on the Re-Opening, Common Prosperity, and Taiwan.

China: The Good, the Bad, and the Pragmatic

Before the pandemic, FEG staff regularly traveled to China and other major Asian markets to better understand the investment opportunities and risks of the region, and to source skilled investment managers in markets outside the U.S. A lot has changed in China in the past three years. China and the U.S. are in the midst of a contentious trade war which includes restrictions on certain tech transfers; China’s zero-COVID policy during the pandemic had devastating economic consequences from which the country is trying to recover; tensions between China and Taiwan have worsened; and President Xi has signaled that he does not intend to relinquish power by announcing an unprecedented third term—only Chairman Mao served as long, and that was in part because he had no obvious successors. It is no wonder, then, investors are wondering whether China is still investable. This report breaks down what is still good in China, what is bad, and how investors might want to engage with the Chinese markets from a practical standpoint.

The Good

The good is still amazing. China is a big, inefficient market with many fast-growing companies in cutting-edge industries. Having approximately 1.5 billion people operating under a leader determined to modernize and compete on the global stage is powerful.1 Take Shenzhen for example. Shenzhen was one of China’s first planned cities when the government began reforming the country’s economy. Today it has a population of more than 17 million, but 40 years ago the population was less than 1% that size.2 Some of the largest and most impactful Chinese companies, including Baidu, Tencent, Huawei, DJI, and ZTE, have offices or are headquartered in Shenzhen. The city also has one of China’s three major stock exchanges on which thousands of companies trade, providing deep and liquid markets for local and foreign investors.

Yet, Chinese equities trade at lower multiples and remain largely inefficient relative to other large markets. The MSCI China Index was trading at a forward price-to-earnings ratio (P/E) of less than 11x as of June 30, 2023.3 In comparison, the S&P 500 Index was trading at more than 20x.4 It gets even cheaper when comparing valuations to growth. Using a P/E-to-growth (PEG) ratio, which is the forward P/E ratio divided by growth, China was trading at less than 0.5x, versus more than 1.6x for the S&P 500 Index.5 Those are significant discounts for a market that is one of the only true competitors for the U.S. from a technological and innovation perspective.

One area in which China is leading the world is electric vehicle (EV) penetration. China recently became the world’s leader in auto exports, passing Germany and Japan, due in large part to the massive growth in global demand for EVs. EV penetration in China is now up to 30% and could reach 50% soon.6 That figure is world-leading—years ahead of both the European Union and the U.S. Furthermore, with EVs also comes the need for infrastructure, and there are significantly more charging stations in China, as the country’s investment in infrastructure dwarfs that of the U.S. The world is turning green, and China, through EVs and solar, seeks to dominate global production.

It is also remarkable how Chinese highways and city streets are dominated by domestic car brands. The increased number of cars from manufacturers like BYD Auto, Geely Auto, Great Wall Motor, and Li Auto since the last time FEG had boots on the ground in China was glaring. FEG staff rode in several of them. They had the technology of a Tesla but at a lower price point. It is obvious why General Motors announced layoffs and cuts within its China business.

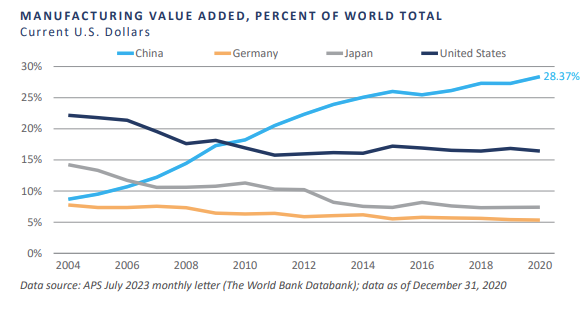

Expanding on the manufacturing topic, China has largely been considered the world’s leader in manufacturing for years. China generates more than a quarter of the world’s manufacturing output—approximately as much as the U.S., Japan, and Germany combined,7 and is now moving into advanced manufacturing. For example, several domestic Chinese companies are trying to play catch-up in the semiconductor chip technology space. China is still working to progress in advanced semiconductor chips, which could be up to 10 years behind competitors. While friend-shoring and supply chain diversification are real, no country can quickly replace China’s manufacturing capacity. Training workers and building factories, ports, roads, and railheads can take years. For example, Apple announced it is opening production in India. It will take several years and billions of dollars, but India will likely still be a minority producer of Apple products, and that is only if everything goes to plan. Therefore, it is likely China will retain its status as “the world’s factory” for years to come.

Artificial intelligence (AI) is another exciting area of opportunity in China. This theme has recently become a dominant theme driving markets and been an area to which businesses have had to devote significant resources to better understand how AI can influence their companies. At present, there are only two countries leading the way in AI: the U.S. and China. While the U.S. may have taken the early lead with generative AI like ChatGPT, Chinese tech leaders like Baidu, Tencent, and others are launching their own versions—e.g., ERNIE. Investors may also see Chinese AI more focused on areas where the country is already a leader, such as manufacturing AI or autonomous driving.

One of China’s biggest advantages is its access to data. Deep learning models need data, and China has a lot of it. The country has an immense population and the government has collected an enormous amount of data via its large number of surveillance apparatuses.

The Bad

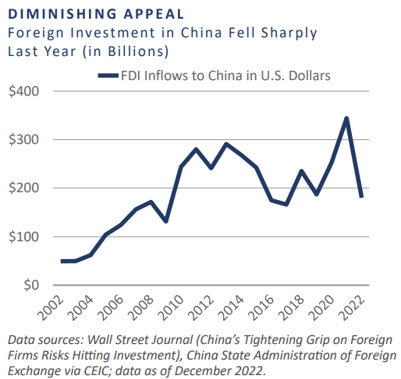

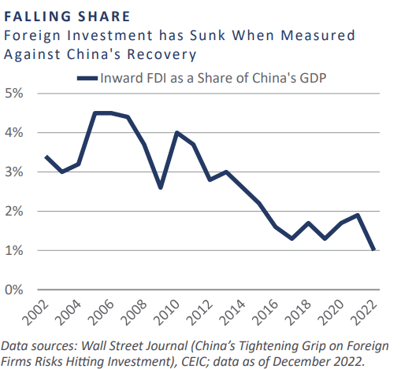

China is an authoritarian state and has externally projected a more hawkish stance under President Xi. The forced transfer of (or stolen) corporate intellectual property, raids on U.S.-based consulting firms working in China, and China’s general policy on Taiwan have all contributed to more contentious relations between China and the U.S. Certain U.S. technologies that could be used by the Chinese military are already prohibited. And while no comprehensive policy is in place, some politicians have suggested the U.S. should go further with the outright banning of U.S. investment into China. Regardless of valuations, this has led many to ask the key question: Is China investable?

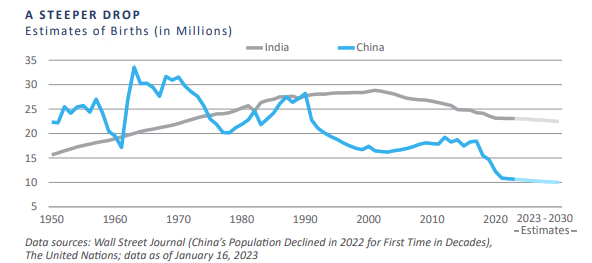

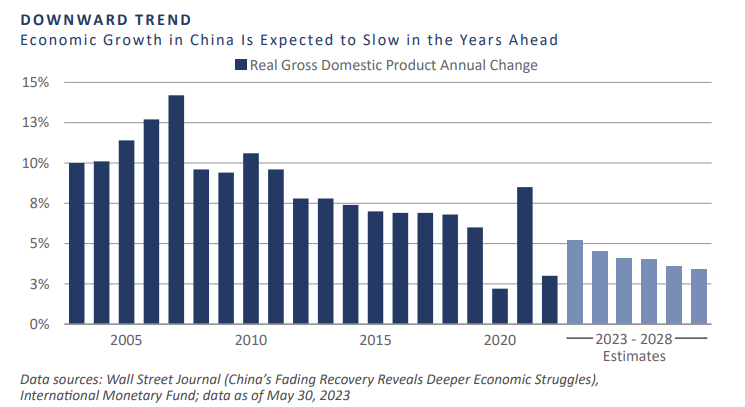

In April this year, India officially surpassed China in terms of total population, and according to projections from the United Nations, the population gap between the two countries is expected to grow precipitously over the next 30 years.8 This shift can largely be attributed to China’s one-child policy, which was implemented when the country was much poorer, and its population was growing too fast. Limiting Chinese families to one child was effective in slowing population growth, but it resulted in a smaller and older society. Given that China no longer offers the same attractive demographics it once did, the question is whether there is enough youthful vibrancy left for the country to achieve its goal of transitioning to more of a consumer and service economy. Investors are left to weigh the risk of whether China will grow old before it can become rich.

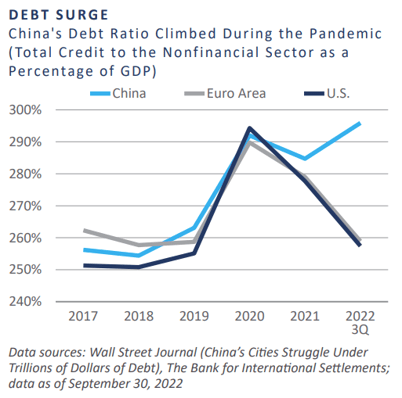

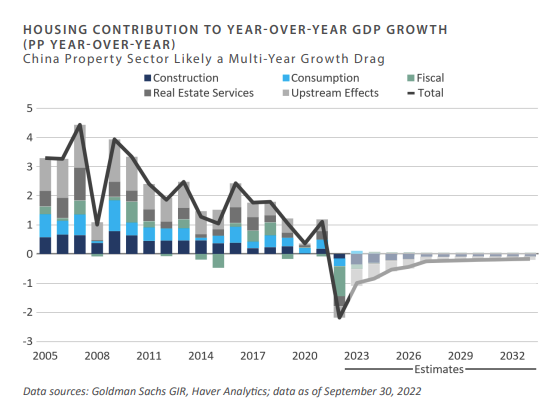

Another negative is that China has a lot of bad debt. The beginning of China’s rise was fueled by a massive infrastructure boom. As mentioned earlier, Shenzhen skyrocketed from a small fishing village to a city of 17 million people in only a few decades. The first airport or train line in a growing city or region is enormously stimulating, but by the fifth or sixth airport, the impact is much less noticeable. To help fuel China’s infrastructure buildout, the government kept interest rates low. Also, most types of consumer investments were limited to property. With low interest rates and limited investment options, consumers poured into speculative property investment. This has led to massive amounts of debt among many banks and property developers. The Chinese government has recognized this debt overhang and tried to manage it, but the debt does limit some potential stimulus responses.

The Pragmatic

So how can investors best handle the good and bad that go along with considering an investment in China? A pragmatic approach is the best bet. China is the world’s second-largest economy, comprising approximately 3% of the MSCI All Country World Index (ACWI) and nearly 30% of the MSCI Emerging Markets Index.9 This makes it challenging to completely avoid. Some investors have opted to divest from China to help reduce problems that could arise from new regulations or geopolitical fallout. While this is a viable option, it can introduce significant tracking error within an equity portfolio that measures performance against benchmarks like the MSCI ACWI or MSCI Emerging Markets Index. For example, the iShares MSCI Emerging Markets ex-China ETF has a tracking error versus the MSCI Emerging Markets Index of more than 9% over the trailing three- and five-year periods.10 That indicates the MSCI Emerging Markets Index is no longer a suitable benchmark. Instead, FEG recommends that investors consider incorporating such decisions into their investment policy statement and adjusting their benchmarks to ones that also exclude China.

For those who feel the good is worth the risk, FEG recommends investing in liquid stocks. As one manager suggested, “Take Chinese valuations and discount potential issues surrounding growth and any sanctions. If the market is still cheap, consider buying Chinese stocks but maintain liquidity.” If the dynamics change, there may be a targeted ban on certain key sectors or industries, and investors will be given time to exit their positions; this has been the modus operandi of the U.S. government thus far. FEG also recommends investors consider avoiding politically sensitive companies. The U.S. government is unlikely to worry about a domestic retailer or insurance company in China, but they could have concerns about a company developing facial recognition AI that could be used by the military. This means China may be more of an alpha opportunity than a beta play.

FEG believes one area to be particularly careful about investing in is private investments. The largest component of private investing in China is venture capital. Venture capital often involves cutting-edge technology. While private equity valuations have come down, and China offers lots of innovation, these are long-term investments. Venture capital can often have holding periods of 10 to 12 years. This means investors are making a bet that relations between the U.S. and China do not escalate. If they do, these investments may have a significant risk of loss. Therefore, FEG believes only investors with a high risk tolerance should consider private investments in China.

Although China-U.S. relations are strained at present, they have evolved over the years and will continue to evolve. FEG is hopeful that cooler heads will ultimately prevail to avoid any major confrontations. As with any fluid situation, investors will need to stay informed and agile.

Re-Opening Observations

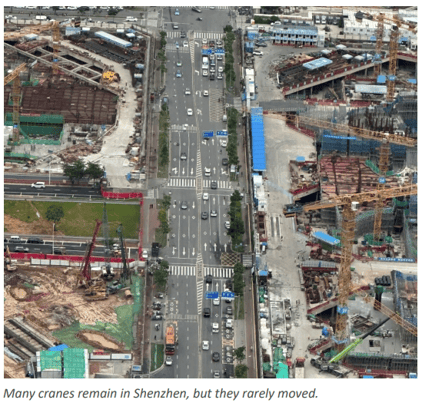

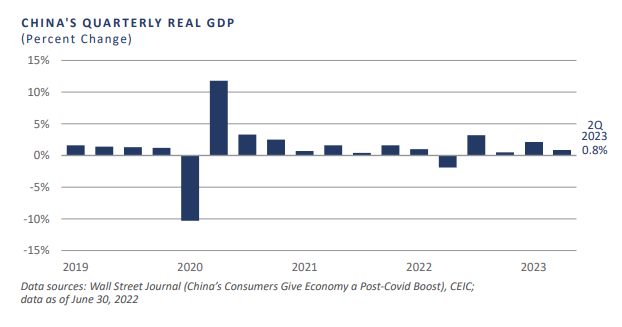

While China is still a place of wonder, FEG's on the ground experience was mixed after so many years away. The infrastructure is still impressive, and construction is ongoing, but the buzz was not as dramatic. There were lots of people, yet it felt less bustling. The traffic was bad, but not as bad as it used to be. These observations are supported by China’s economic activity following the lifting of pandemic restrictions, which has been disappointing relative to expectations.

The weaker rebound from pandemic restrictions relative to other markets is likely due in part to cultural differences. The U.S. is a country of consumers, but the Chinese tend to be more cautious. It is also worth pointing out that the U.S. re-opening was not a straight line, as the country continued to endure multiple COVID-19 variants in the ensuing months. Rather than engaging in explosive so-called “revenge spending,” Chinese consumers have increased their savings and paid down debts. Another difference is the Chinese government has the capacity to be more stimulative than most other developed countries when economic activity sputters. They need to be careful not to restimulate a property bubble, but they do have options at their disposal. This is only a short-term observation, and FEG is a long-term investor. However, in the short-term, the Chinese re-opening boom seems underwhelming.

Common Prosperity

There has been significant coverage in Western media on the impact of the new common prosperity policy, but there needs to be more clarity about its meaning. Many outside the country interpret this new policy as a communist crusade against capitalism in China, which is likely a bridge too far. The primary emphasis from the Chinese perspective is everyone should have the opportunity to develop themselves and contribute to society.

Common prosperity was only a small portion of the broader 104,000-page policy document prepared for the latest Party Congress. In fact, it appears only six times in those pages.11 Yes, it is a part of the new Party Policy, but only a part, not the focus.

It is absolutely possible the Chinese Communist Party will redistribute more wealth in the future, but this is probably needed. China’s wealth gap has grown significantly over the past 30 years,12 and the country has no social safety net like in the U.S., nor does it charge a property or inheritance tax—both of which are levied in the U.S. In fact, the U.S. and Europe both redistribute more wealth to lower-income classes than China does. China’s redistribution ranks around that of Mexico and Turkey, and China is a communist country.

As one manager stated during this recent trip: “Prosperity cannot be made common if there is not prosperity first.” The Chinese Communist Party is not democratically elected; it only has legitimacy if it performs. Systemic stability is paramount. China government officials have studied the collapse of the Union of Soviet Socialist Republics (USSR) and concluded the economy was not dynamic enough to support defense and social spending. Therefore, the Chinese government is focused on maintaining a robust economy but will do so in its own way. The Chinese growth story has pulled an estimated 800 million people out of poverty, but many Chinese citizens are still impoverished, albeit a significantly smaller percentage of the total population than before China’s modernization. With a need for stability and continued progress, Chinese capitalism will look different from U.S. capitalism. Common prosperity is likely to be a defining factor in President Xi’s legacy.

Taiwan

Over the last few years, tensions around the One China Policy’s goal of a unified Taiwan have ramped up. It reached its crescendo around a major Chinese military exercise which appeared to rehearse what a naval blockade might look like. That was precipitated by a visit to Taiwan from then-Speaker of the House, Nancy Pelosi. However, the war between Ukraine and Russia may have pushed off any conflict between China and Taiwan for several years. While Ukraine’s defense against a mightier opponent may have inspired some Taiwanese, it also highlighted how devastating the carnage can be. The devastation of war has been broadcasted globally daily and has shown the Chinese the costs of such a conflict, especially if it is not an immediate success. It would be difficult for China to pursue its goal of common prosperity if the country were sanctioned and cut off from the Western world.

Elections in the U.S. and Taiwan will be telling for what is to come with Taiwan. One thing U.S. politicians and the public seem to agree on is being tough on China. The U.S. and China are unlikely to improve relations before the next presidential election, but hopefully back channels between the two countries can be maintained so the relationship does not worsen. As the world’s two major superpowers, China and the U.S. need to coordinate on many things, and a good relationship would certainly help.

As for the Taiwanese election in January, how the independents vote may have a large impact on the future of Taiwan. Like the U.S., Taiwan is essentially a two-party government; one side is pro-independence and one is more pro-China. In addition to the two organized parties, there are also a large swath of independents in Taiwan, making this group essential in shaping the country’s relationship with China.

1 The World Bank, www.worldbank.org

2 Shenzhen Municipal Financial Centre Development

3 FactSet, www.factset.com

4 FactSet, www.factset.com

5 FactSet, www.factset.com

6 APS Asset Management, www.aps.com

7 The World Bank Databank, www.worldbank.org

8 The United Nations, www.un.org

9 MSCI, www.msci.com

10 eVestment Alliance, www.evestment.com

11 APS Asset Management, www.aps.com

12 APS Asset Management, www.aps.com

13 The World Bank, www.worldbank.org

DISCLOSURES

This report was prepared by Fund Evaluation Group, LLC (FEG), a federally registered investment adviser under the Investment Advisers Act of 1940, as amended, providing non-discretionary and discretionary investment advice to its clients on an individual basis. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser.

The information herein was obtained from various sources. FEG does not guarantee the accuracy or completeness of such information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. FEG assumes no obligation to update this information, or to advise on further developments relating to it.

Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell any securities.

Any return expectations provided are not intended as, and must not be regarded as, a representation, warranty or predication that the investment will achieve any particular rate of return over any particular time period or that investors will not incur losses.

Past performance is not indicative of future results.

This report is prepared for informational purposes only. It does not address specific investment objectives, or the financial situation and the particular needs of any person who may receive this report.

Fund Evaluation Group, LLC, Form ADV Part 2A & 2B can be obtained by written request directed to: Fund Evaluation Group, LLC, 201 East Fifth Street, Suite 1600, Cincinnati, OH 45202 Attention: Compliance Department.

CFA: The Chartered Financial Analyst® (CFA) designation is a professional certification issued by the CFA Institute to qualified financial analysts who: (i) have a bachelor's degree and four years of professional experience involving investment decision making or four years of qualified work experience[full time, but not necessarily investment related]; (ii) complete a self-study program (250 hours of study for each of the three levels); (iii) successfully complete a series of three six-hour exams; and (iv) pledge adhere to the CFA Institute Code of Ethics and Standards of Professional Conduct.

The Charted Alternative Investment Analyst Association® is an independent, not-for-profit global organization committed to education and professionalism in the field of alternative investments. Founded in 2022, the CAIA Association is the sponsoring body for the CAIA designation. Recognized globally, the designation certifies one's mastery of the concepts, tools and practices essential for understanding alternative investments and promotes adherence to high standards of professional conduct.